Liv-ex December Market Report

- All major fine wine indices dipped in November, while US and UK stocks rebounded.

- Tuscany’s monthly trade share reached a record high for the year.

- Soldera Case Basse and Masseto drove the Italy 100 index to close November as the only Liv-ex 1000 sub-index in positive territory.

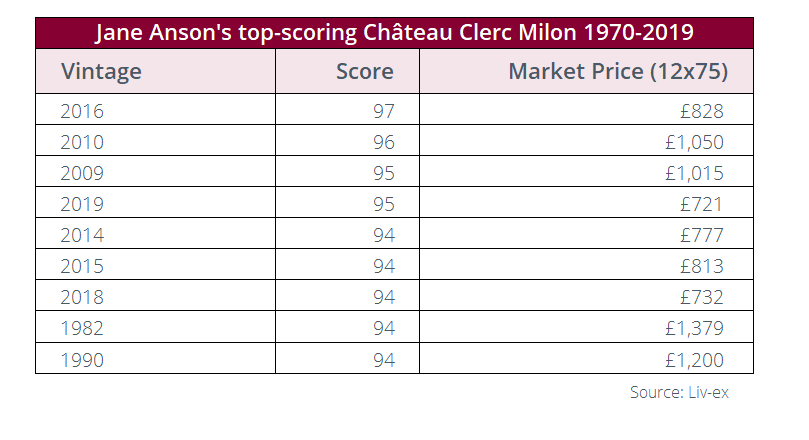

- In a vertical tasting of Château Clerc Milon, Jane Anson awarded the 2016 vintage her highest score.

- While the 162nd Hospices de Beaune auction of Burgundy 2022 hit a new record, Burgundy’s price gains have slowed over the course of the year.

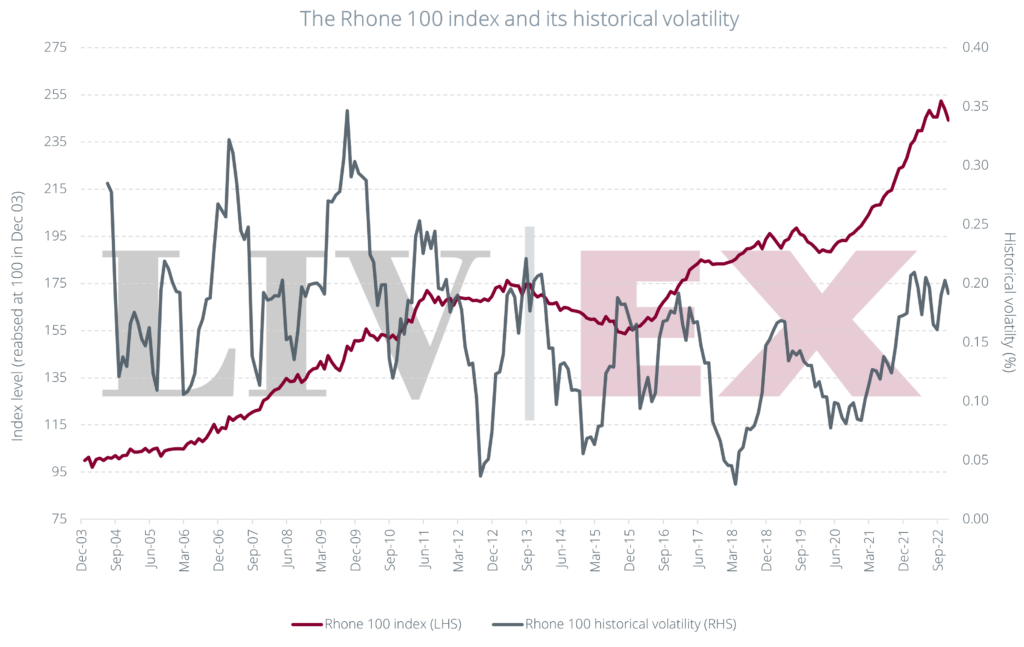

- The Rhône 100 index has risen 7.0% so far this year, while showing the lowest historical volatility compared to other regions.

Equities rebound but fine wine dips in November

Global equities rebounded in November, with the S&P 500 rising 6.3% and the FTSE 100 up 7.3%. This comes as inflation showed signs of slowing and central banks are forecast to slow the pace of interest rates. The bullish sentiment might continue into December, which has historically been one of the best months for US stocks. However, market volatility remains high due to monetary policy tightening and China’s on-going (though less severe) zero-covid policy.

While equities rose, fine wine prices slipped last month. The Liv-ex Fine Wine 100 index fell for the second consecutive month, down 0.4%. The strengthening of Sterling brought the index’s rally to a halt. First Growth prices were also affected, with the Liv-ex Fine Wine 50 index falling 1.1%.

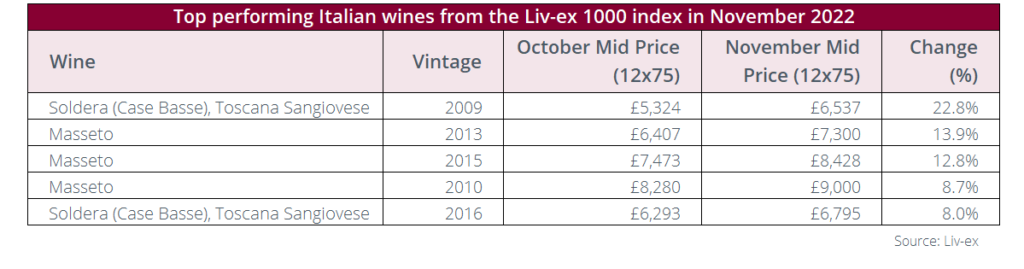

The broadest measure of the market, the Liv-ex 1000 index, declined 0.6%. Only one of its sub-indices rose in November: the Italy 100 was up 0.6%. The best-performing Italian wines were the Tuscans Soldera Case Basse Sangiovese 2009 and Masseto 2013.

Meanwhile, the Champagne 50 was the worst performer, down 2.5%. The biggest fallers were two of the most in-demand Champagnes this year – Salon Le Mesnil-sur-Oger Grand Cru 2012 (-12.0%) and Louis Roederer Cristal 2008 (-10.0%).

Chart of the Month

November proves best month for Tuscan trade

Tuscany’s trade share in November reached a record high for the year at 8.1% of the total market by value. The region’s trade was spearheaded by the 2019 vintage, especially Super Tuscans Sassicaia and Tignanello.

The region has been in the critical spotlight this month, with new reports from publications like The Wine Independent, along with the En Primeur launch of the 2018 Brunello di Montalcinos.

Champagne continued to enjoy heightened demand, with its share rising slightly from 18.1% in October to 18.7% in November. Louis Roederer Cristal 2014 and 2008 were its most active wines.

Meanwhile, Bordeaux (30.8%) dipped and accounted for an almost equal share as Burgundy (30.0%). The First Growths made up 28.9% of all Bordeaux trade.

Piedmont (1.9%) and the ‘others’ (3.4%) also lost market share in November. Trade within the latter was dominated by Australia (0.8%) and Spain (0.7%).

Biggest Risers this month

Top performers from Tuscany

Along with its record market share, November was also a strong month for Tuscany in terms of price performance. The region propelled the Italy 100 index this month, resulting in it being the only sub-index of the Liv-ex 1000 to end the month in positive territory.

Two labels were at the forefront of these price increases: Soldera (Case Basse), thanks to its Sangiovese 2009 and 2016, and Masseto, with its 2010, 2013 and 2015 vintages. The wines have set new trading records this year and are currently at their highest levels. The 2015 Masseto, which jumped 12.8% in value, also carries a 100-point score from The Wine Advocate’s Monica Larner. She described it as ‘absolutely teeming with sensorial spirit that is transmitted through the bounty of the bouquet and the solid tannins of the mouthfeel’.

Critical Corner

Jane Anson’s vertical tasting of Château Clerc Milon

Château Clerc Milon has been a Pauillac property on the move in the secondary market. All of its last 10 vintages have risen in value this year, with the 2010 (21.4%), 2019 (18.6%) and 2016 (18.3%) leading price performance. The three vintages have also set new trading records in the last quarter.

Jane Anson (Inside Bordeaux) recently looked back at the evolution of the estate, through a vertical tasting spanning 50 years (1970-2019). She noted that during this time ‘the vineyard changed in size and shape’, while ‘winemaking teams, cellar equipment and vintage conditions’ also evolved. Anson had previously suggested that the Fifth Growth is of Third Growth quality in her own JA ranking in her Inside Bordeaux book.

She said in her report: ‘While it was certainly true that from 2010 onwards Clerc Milon began its vertical rise to the exceptional position that it occupies today, what was striking in this tasting was how clearly its personality shone through from beginning to end’.

Her highest-scoring wine was the 2016 vintage, which she described as ‘a profound wine that shows the possibilities contained within this site’. The most traded Clerc Milon in the past year, the 2019, received 95-points from the critic. She noted that it was ‘Jean Emmanuel Danjoy’s last full vintage before he headed over to Mouton Rothschild in 2020’.

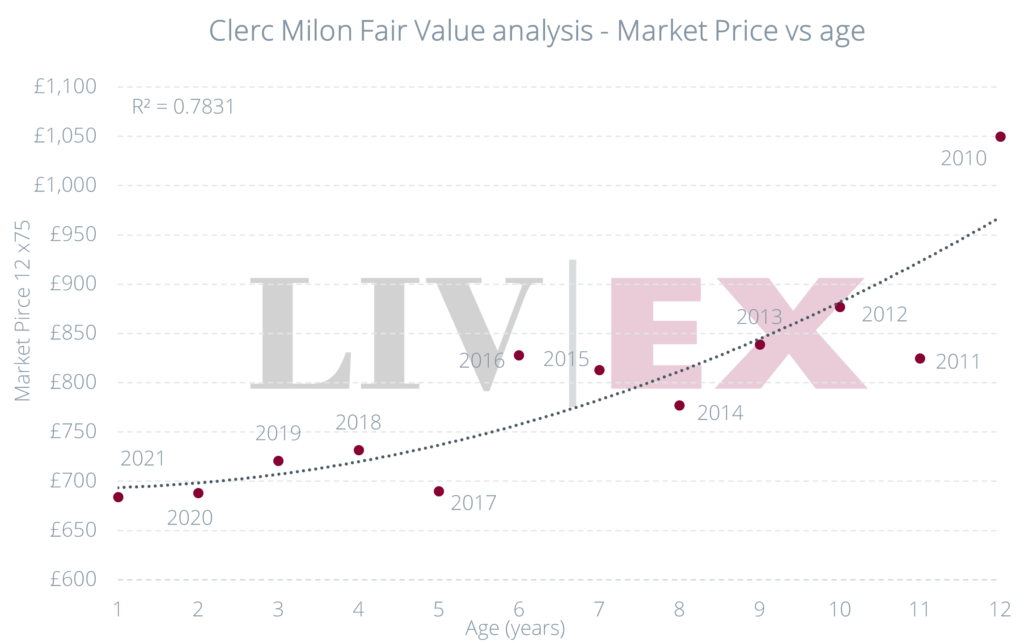

Clerc Milon prices show stronger correlation to age (78%) than critic scores. As the chart below shows, the 2014 vintage, which Anson awarded 94-points, represents relative value. The 2011 and 2017 also look attractive based on bottle age. Most of Clerc Milon’s recent vintages remain available around £800 per case, with prices rising over time.

News Insights

Secondary market sentiment for Burgundy following auctions

The 162nd Hospices de Beaune wine auction this November raised €31 million, setting a record that is twice that of the previous one set in 2018.

On offer were 802 barrels drawn from 51 cuvées, representing a significant increase on the 2021 auction, which featured 362 lots due to the historically low crop. This year, the ‘Pièce des Présidents’ barrel also achieved a record-breaking price, selling for €810,000. According to Meininger’s WBI, 700 people ‘physically attended the seven-hour auction, but bids were also placed by telephone and online from 30 countries worldwide’.

The news tells a story of unprecedented levels of demand and soaring prices, but on the secondary market sentiment for Burgundy has started to falter. As our end of year report points out, Burgundy’s bid:offer ratio (a measure of market sentiment) has fallen to 0.3, below the market average of 0.4. In practice, this means that more people are offering Burgundy stock than are willing to buy it, putting pressure on the asking prices.

Burgundy’s price gains have also slowed over the course of the year. The Burgundy 150 index rose 14.6% in the first quarter, compared to a 1.7% increase over the last three months. The index then fell 0.9% in November. Meanwhile, total trade value dropped 15.0% over the past three months, compared to Q1 2022, while volume trade went down 19.6%. While Burgundy’s performance continues to be unmatched by any other fine wine region, such figures show that no market can rise forever.

Final Thought

Finding quality and stability in the Rhône

The Rhône attracted significant critical attention in November, with Jancis Robinson publishing a series of articles on the 2021 vintage and Jeb Dunnuck reviewing the 2018 and 2019s from the northern appellations. This was reflected in the region’s secondary market activity, which increased last month.

Year-to-date, it has been the 2019 (16.4%) and 2018 (14.9%) vintages that have led the region’s trade. Châteauneuf-du-Pape (54.7%), Côte-Rôtie (19.0%) and Hermitage (16.7%) have been the most-traded appellations.

The Rhône resists market pressure from Burgundy and Champagne

Of the leading regions traded on the secondary market, the Rhône has been the least affected by the rising dominance of Burgundy and Champagne. While its trade share year-to-date (4.0%) has been lower than the 2021 average (4.5%), it has declined less than that of Bordeaux, Tuscany, Piedmont and California, which have all been impacted by demand for the two French regions.

The Rhône has remained extremely stable – both in terms of trade and prices. As our 2020 report on the region highlighted, the Rhône has been ‘solid as a rock’. With consistently high scores, healthy production volumes, market availability and relative value.

Rising prices, low volatility

In terms of value, the Rhône has continued to represent the lowest entry point into the fine wine market. However, prices have been on the rise; the Rhône 100 index is up 7.0% so far this year, outperforming the California 50 (6.3%), Bordeaux 500 (6.1%) and the Rest of the World 60 (5.4%).

Historically, its index has also experienced the lowest volatility.

Historical volatility measures how much an index has deviated from its moving average. This is calculated based on a six-month moving average, and month-on-month index returns. We then calculate how much the index level differs from its six-month moving average. The monthly volatility is then converted into an annualised figure, by multiplying the monthly standard deviation by twelve.

In general, the lower the volatility the lower the risk. This is because the index prices depart less from the moving average.

Over the last three years, the Rhône 100 index has risen 27.4% and has shown an average annualised volatility of 13.8%. With a smaller increase of 21.2%, the Bordeaux 500 index volatility has been 10.2%. By contrast, the Burgundy 150 index has increased 62.9% but its volatility has also been one of the highest at 25.2%.

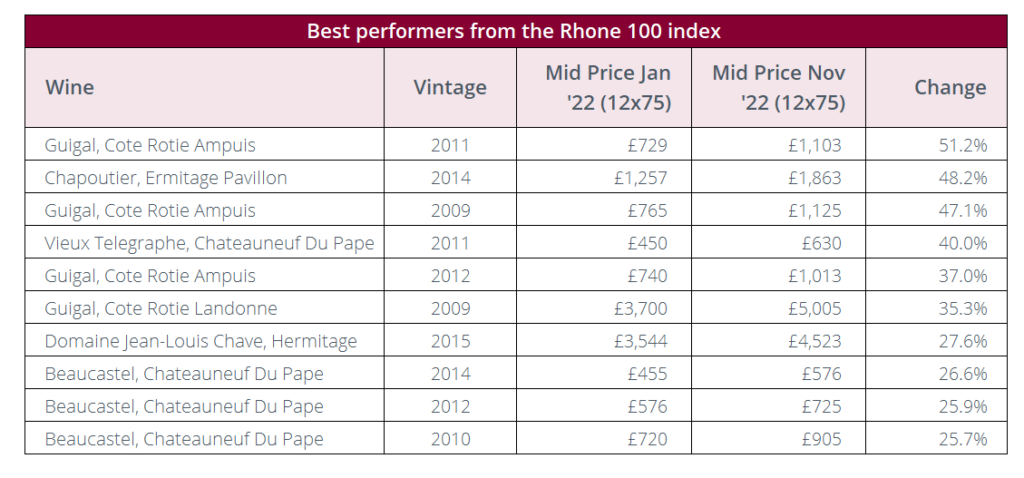

The best-performing wines from the Rhône

Some wines within the index have delivered impressive price performances this year. The biggest risers in the table above have all risen between 25.7% and 51.2%. These include six wines from the northern Rhône, and four from Châteauneuf-du-Pape in the south.

E. Guigal Château d’Ampuis 2011 has led the way, with its 2009 (47.1%) and 2012 (37.0%) in leading positions. In the 2022 Power 100 rankings, E. Guigal was the third highest-ranked brand by volume traded.

The top-ranked Rhône label in the Power 100 was Michel Chapoutier, driven by a high number of different wines trading. Meanwhile, Château Rayas re-entered the top 100 with a jump of 55 places thanks to a strong average trade price and price performance.

While the Rhône remains one of the quieter secondary market players, the region delivers an embarrassment of riches.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600 merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £80m of bids and offers across 16,000 wines.