Print and read offline instead.

In this report:

- The Liv-ex 50 and Liv-ex 100 declined in July, demonstrating that the pressures of the wider global economic outlook are starting to weigh on fine wine to an extent.

- Champagne’s trade share by value hit a record high of 16.7% of the total market.

- Unlike the other estates in the Rest of the World 60 index, none of Vega Sicilia ‘Unico’ wines dropped in value last month.

- In a Bordeaux 2005 retrospective, Lisa Perrotti-Brown MW awarded seven wines 100 points.

- The secondary market for Australian wine has continued to shrink as export volumes fall.

- The most accessible entry points into fine wine, Sauternes and Port, have seen the smallest changes to their average price since 2019 and remain under £1,000 per case on average.

Champagne keeps rising in July as economic pressures mount

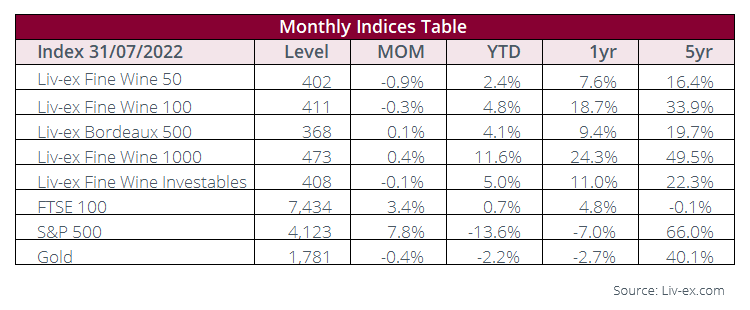

The Liv-ex Fine Wine 100 declined in July for the first time in over two years, dipping 0.3%. The index had enjoyed a 24-month run of rises from June 2020 to June 2022, rising 36.1% in that time.

The Fine Wine 50, which tracks the daily price movements of the Bordeaux First Growths, also declined 0.9%.

Meanwhile, the broadest measure of the market, the Liv-ex Fine Wine 1000, rose 0.4%. Among its sub-indices, the Champagne 50 was up 3.1%, while the Burgundy 150 rose 1.2%. The Bordeaux 500 and Italy 100 largely held steady, rising 0.1% and 0.3% respectively.

The biggest dip was the Rhône 100 which declined 1.1% and the Rest of the World 60, which was down 0.8%. Despite this, all seven sub-indices have risen year-to-date and over the last one, two and five-year periods.

The diversity of the Liv-ex 1000 is undoubtedly its biggest strength and demonstrates the greater resilience of the secondary market when faced with external pressures.

Nonetheless, the performance of these three key indices demonstrates that the pressures of the wider global economic outlook are starting to weigh on fine wine to an extent.

Divining any firm directional shifts is difficult in the traditionally quieter summer months. However, rising inflation and fears of recession are undoubtedly setting the scene for a testing autumn and winter period.

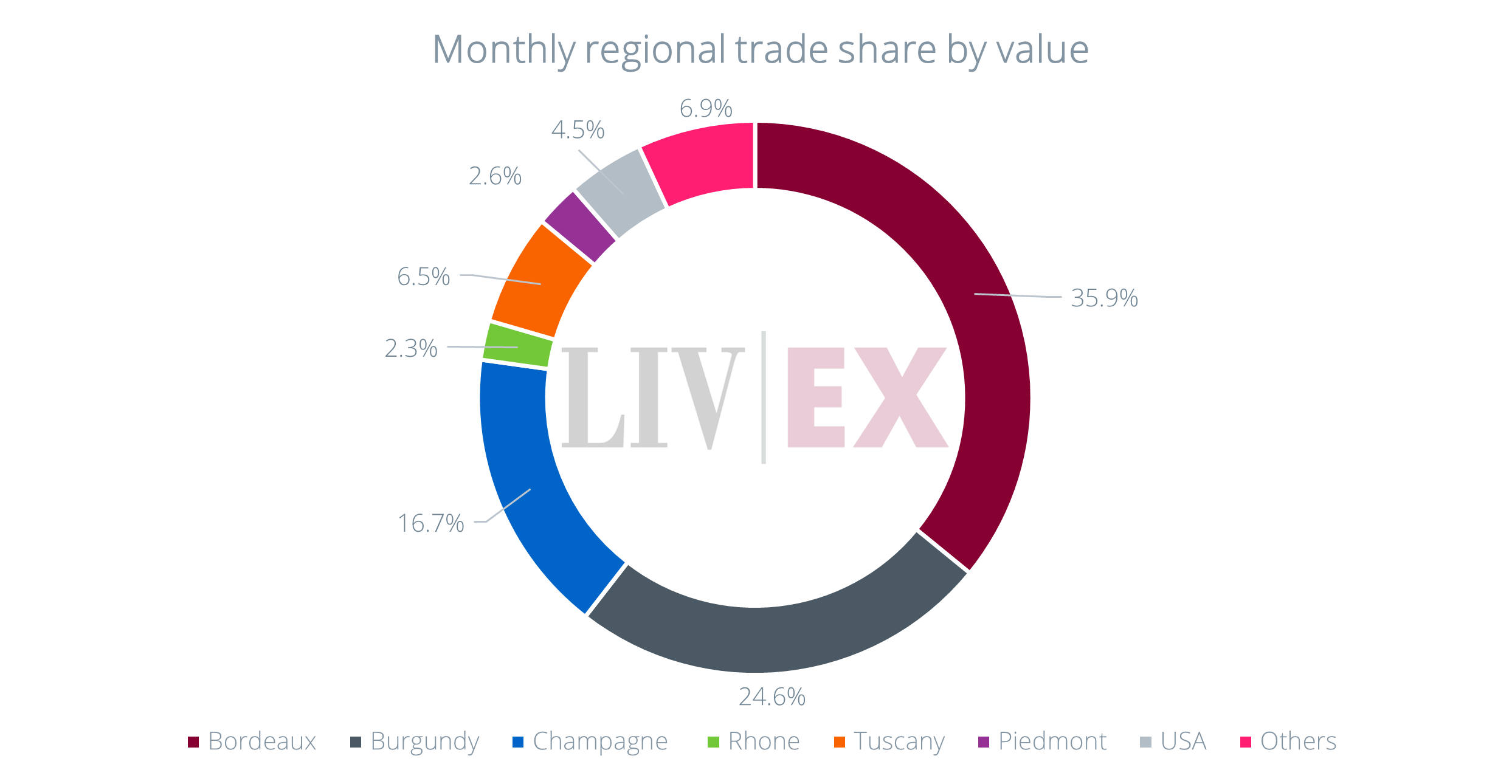

Chart of the month – Champagne’s monthly trade share reaches a record high

Champagne’s trade share by value hit a record high in July of 16.7% of the total market. The previous peak was set in May 2021, when the region accounted for 13.2% of all trade, driven by increased demand for rosé. Last month, 175 different Champagnes (LWIN11s) changed hands. The 2008 and 2014 were the most active vintages, and Louis Roederer Cristal was the most traded wine.

Most other regions’ trade share declined compared to June. Bordeaux took 35.9% of the market, led by its 2019 and 2009 vintages. Burgundy’s share dipped from 27.9% to 24.6%, the Rhône from 4.5% to 2.3%, and the USA from 5.1% to 4.5%. Tuscany and Piedmont ran mostly flat. Within the ‘others’, there was demand for wines from Germany (0.9%), Australia (0.8%), Spain (0.7%) and Argentina (0.2%).

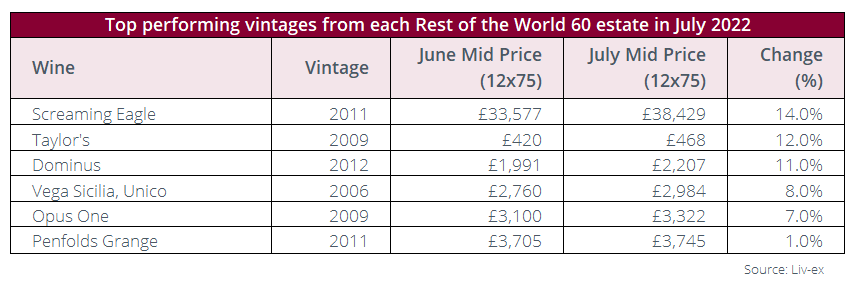

Major Market Movers – Spain’s Vega Sicilia stays positive among Rest of the World 60

Although the Rest of the World 60 index declined in July, not all its component wines experienced a drop in value.

Overall, just under half of the 60 wines in the index either held or rose in value in July, with the other half declining, on balance leading to an under-performance of -0.8%. The best-performing wines from each estate can be seen in the table above.

Screaming Eagle’s 2011 vintage saw the biggest increase, up 14%. It was followed by Taylor’s Port with a rise of 12%.

Unlike the other estates in the Rest of the World 60 index, none of Vega Sicilia ‘Unico’ wines dropped in value last month. The 2011’s price remained unchanged from June and all other tracked vintages rose. The 2006 was its top riser, up 8.0%.

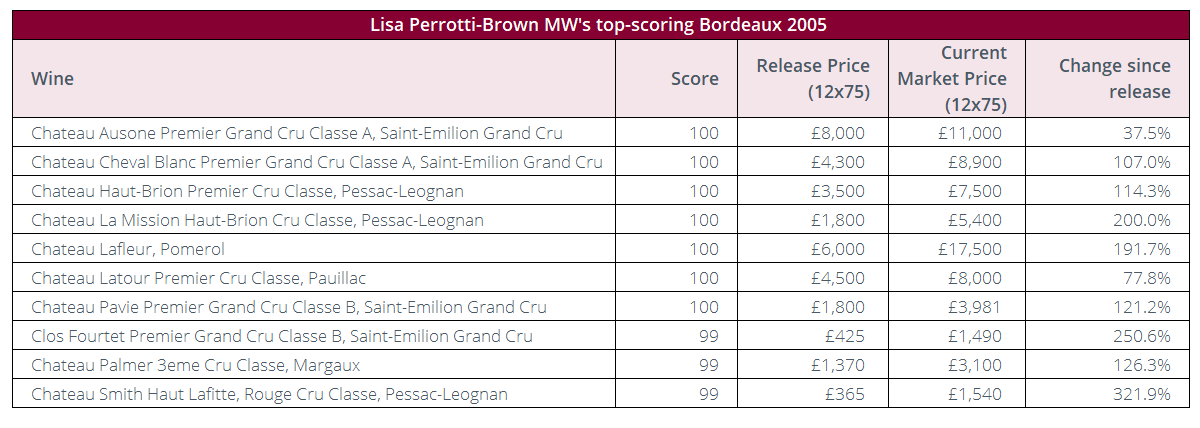

Critical Corner – Lisa Perrotti-Brown MW finds seven 100-point ‘sleeping beauties’ in Bordeaux 2005

Lisa Perrotti-Brown MW (The Wine Independent) has released a Bordeaux 2005 retrospective, following a charity tasting in Nashville and extensive tastings in Bordeaux. In her report, she called it ‘undoubtedly one of the greatest vintages of the 21st Century’.

In total, Perrotti-Brown awarded seven Bordeaux 2005s perfect 100-point scores, as the table below shows. Most of her top-scoring wines have enjoyed triple-digit growth since release.

She added that 2005 is, ‘one of those happy exceptions’ when a ‘great Sauternes vintages coincides with a great red Bordeaux year’.

Balancing high tannins

Perrotti-Brown recalled the high tannins in the reds when tasting the barrels samples in the spring of 2006. She said that it was ‘a great year in the making, but the nascent wines were so tannic and impenetrable that it was difficult to maintain my usual pace of tasting’.

Furthermore, ‘after bottling, most of the wines immediately shut down, falling into a long slumber’. But ‘now, as many of these sleeping beauties begin to awaken, we can see compelling red fruit and floral accents among the black fruit layers, with savory and mineral nuances’.

She noted that some wines ‘will need a few years yet to hit their stride’ such as Cheval Blanc, Ausone, Haut-Brion, Le Pin, Petrus, Palmer, Montrose, Latour, and Yquem.

Perrotti-Brown said that ‘many top names turned out to be as impressive as I suspected […] but a few others surpassed my expectations’.

She called Clos Fourtet, Rauzan-Segla, Smith Haut Lafitte, and La Gaffelière ‘real jaw-droppers with a long life ahead,’ while pointing out the value for money they offer ‘considering the quality’.

There are currently over 200 Bordeaux 2005 live opportunities on the Liv-ex exchange.

Prices and scores

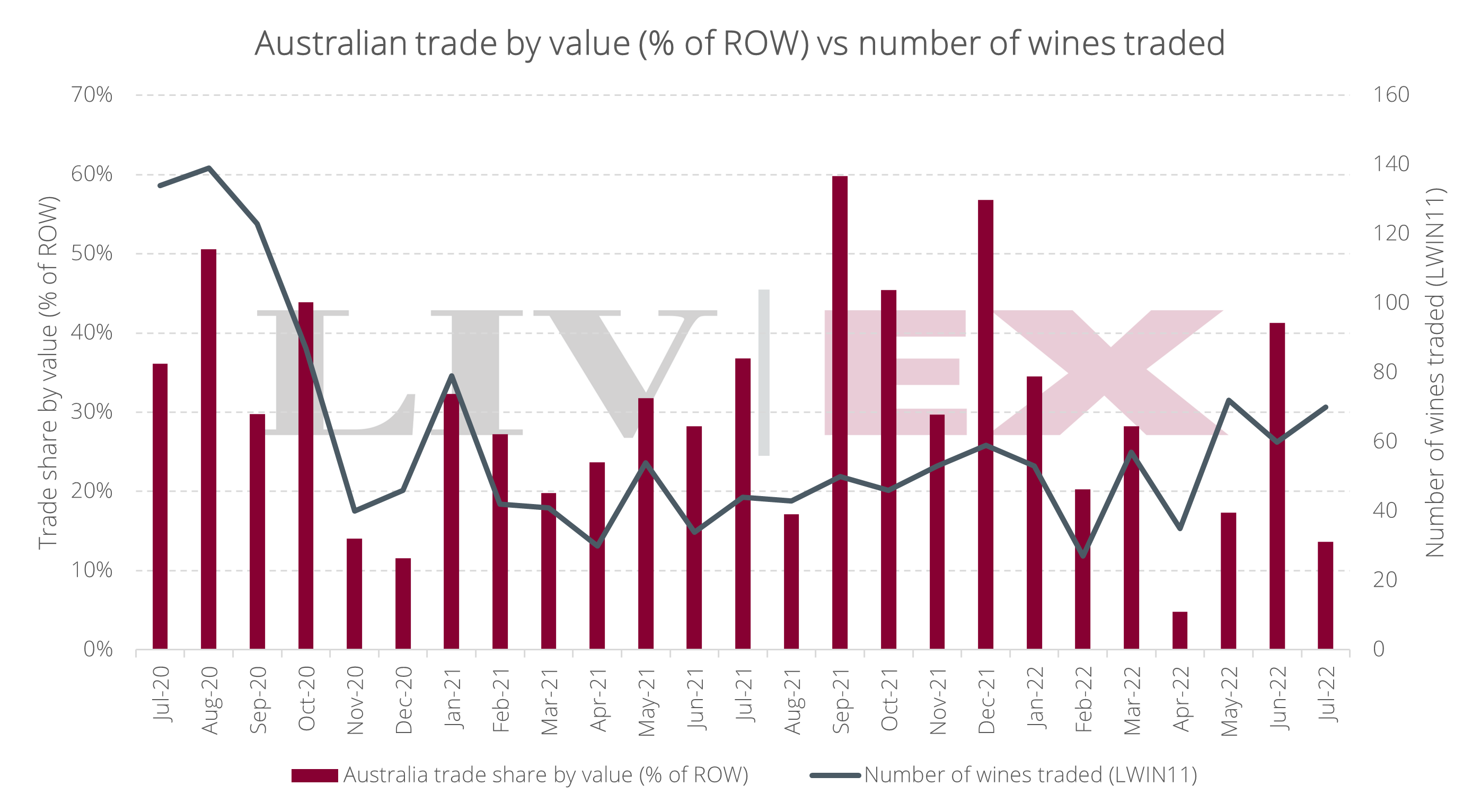

News Insight – The market for Australian wine continues to shrink

In a recent article, the Drinks Business reported that ‘Australian wine has seen AUD$2.08 billion wiped off the value of exports over the last 12 months as the China tariff crisis continues’.

The tariffs, first introduced in November 2020, and updated and formalised in March 2021, range from 116% to 218% and are set to remain in place for five years. Wine Australia’s new report has shown that export volumes have ‘fallen by 10% to 625 million litres in the year to 30 June 2022’.

According to the article, the marketing body anticipated the decline and said that ‘the China tariffs would remain “a significant influence” on the moving annual total data of Australian wine exports until late 2022’. The pandemic has exacerbated the pressure, causing ‘severe shipping delays and increased freight costs, along with rising inflation, business costs and interest rates’.

Australia’s secondary market has shrunk too. In 2020, 360 different wines (LWIN11s) traded on Liv-ex. The number fell to 244 in 2021, and year-to-date, 201 wines have changed hands.

Australia’s trade share of the total market sits at an annual average of 1.0% year-to-date, down from 1.1% in 2021 and 1.6% in 2020.

Within the ‘Rest of the World (ROW)’ category, its average trade share has fallen from 34.1% in 2021 to 22.9% year-to-date. While Australia remains the most important Rest of the World player, it is facing stronger competition from other regions such as Spain and Germany, and this reduction in exports is a worsening outlook.

Final Thought – The rising price of fine wine across different regions

The secondary fine wine market has reached new heights over the past two years. Although the Liv-ex 100 closed July down on the previous month, the Liv-ex 1000 was up slightly (0.4%). Both of the leading fine wine indices are at their highest ever levels.

But as prices of the top wines continue to rise, where should investors look when wanting to buy the top wines of the world?

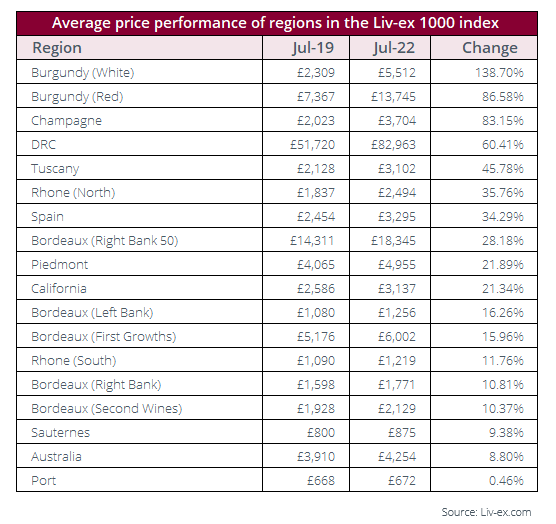

Broadly speaking, the top wines of their respective regions are consistent with the wines that make up our regional indices (i.e. the components of the Liv-ex 1000 index). To give a better idea of the price changes across the secondary market, we have split many of these indices down further, as shown in the table below.

For example, the Rest of the World 60 has been split into California, Spain, Australia and Port. The Rhone 100 has been split into its northern and southern components, and Italy has been divided into Tuscany and Piedmont.

Where wines of great rarity and price might have an impact on the average, we have also kept them separate. For example, Domaine de la Romanée-Conti has been separated from red and white Burgundy and estates in the Right Bank 50 (Pétrus, Lafleur, Le Pin, Ausone and Cheval Blanc) away from the other Right Bank wines.

The final regions can be found in the table below, which shows the average Market Price for each, both now and three years ago.

Unsurprisingly, prices of Burgundy and Champagne have risen the most over the last three years. The Burgundy 150 and Champagne 50 indices have been the best-performers since July 2019, rising 57% and 79% respectively. The Champagne 50 has been out-performing the Burgundy 150 since May 2021.

Cristal, Krug, Dom Pérignon and Salon, have been the main drivers behind Champagne’s rise, with the 2008, 2012 and 2014 vintages being in particularly high demand from the former three.

Meanwhile, white Burgundy’s success has been driven by demand for Montrachet and some of its adjacent appellations such as Chevalier- and Bâtard-Montrachet.

The rising price of Tuscan and Northern Rhône wines also fits the pattern seen in recent years, with both regions finding an increasingly enthusiastic audience who appreciate what they have to offer in terms of quality and value.

The surprising addition so far up the table is Spain – represented by Vega Sicilia ‘Unico’ – which has risen 34.2% in value. As mentioned above, all of the Unico vintages in the Rest of the World 60 at least held their value in July.

Back in 2019, the Californian components of the Rest of the World 60 comprised Opus One and Dominus only. Since then those wines have risen by 21.3% on average. However, Screaming Eagle was added to the index and if we include that estate then the average entry point for Californian wine rises to £14,885 (12×75).

The Bordeaux wines have seen more subdued increases in value. As noted, the region’s trade share has been in decline in recent years. Over the past three years it has accounted for 39.5% of total trade by value.

The most accessible entry points into fine wine, Sauternes and Port, have seen the smallest changes to their average price since 2019 and remain under £1,000 per case on average.

And likewise, both Left and Right Bank Bordeaux as well as wines from the southern Rhône continue to offer wines to potential new buyers that are, on average, under £2,000 a case.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 600 merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 16,000 wines. Independent data, direct from the market.