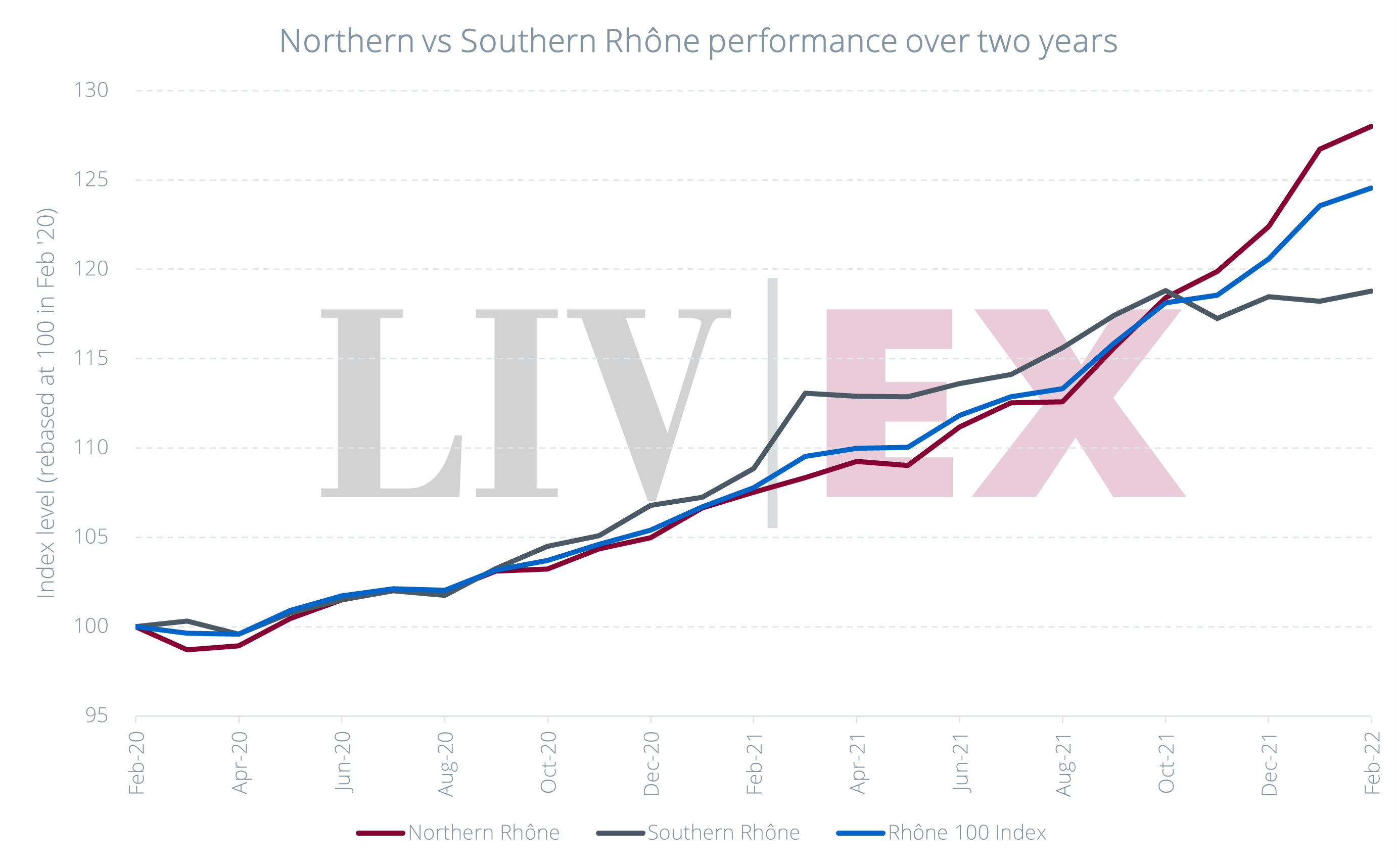

The Burgundy 150 and Champagne 50 sub-indices have led the Liv-ex 1000 over the past two years, but the Rhône 100 index has seen steady price rises, up 24.6% during this period.

The index’s component wines are split between those from the north and south. Looking at the chart below, prices for the more expensive northern Rhône wines in this period have climbed 28.0%, more than those from the south.

While the north and south broadly followed the same path throughout 2020, prices for the southern Rhône peaked in October 2021 and have declined slightly in recent months. However, the northern Rhône has pressed ahead, providing the necessary push to keep the Rhône 100 rising.

Of these northern Rhône wines, Domaine Jean Louis Chave Hermitage Rouge 2014 has been its leading label, rising 78.7% since 2020.

Meanwhile, the wines of Châteauneuf-du-Pape have risen 18.8%. Château de Beaucastel Rouge 2016 has been the top-performer, up 51.8%.

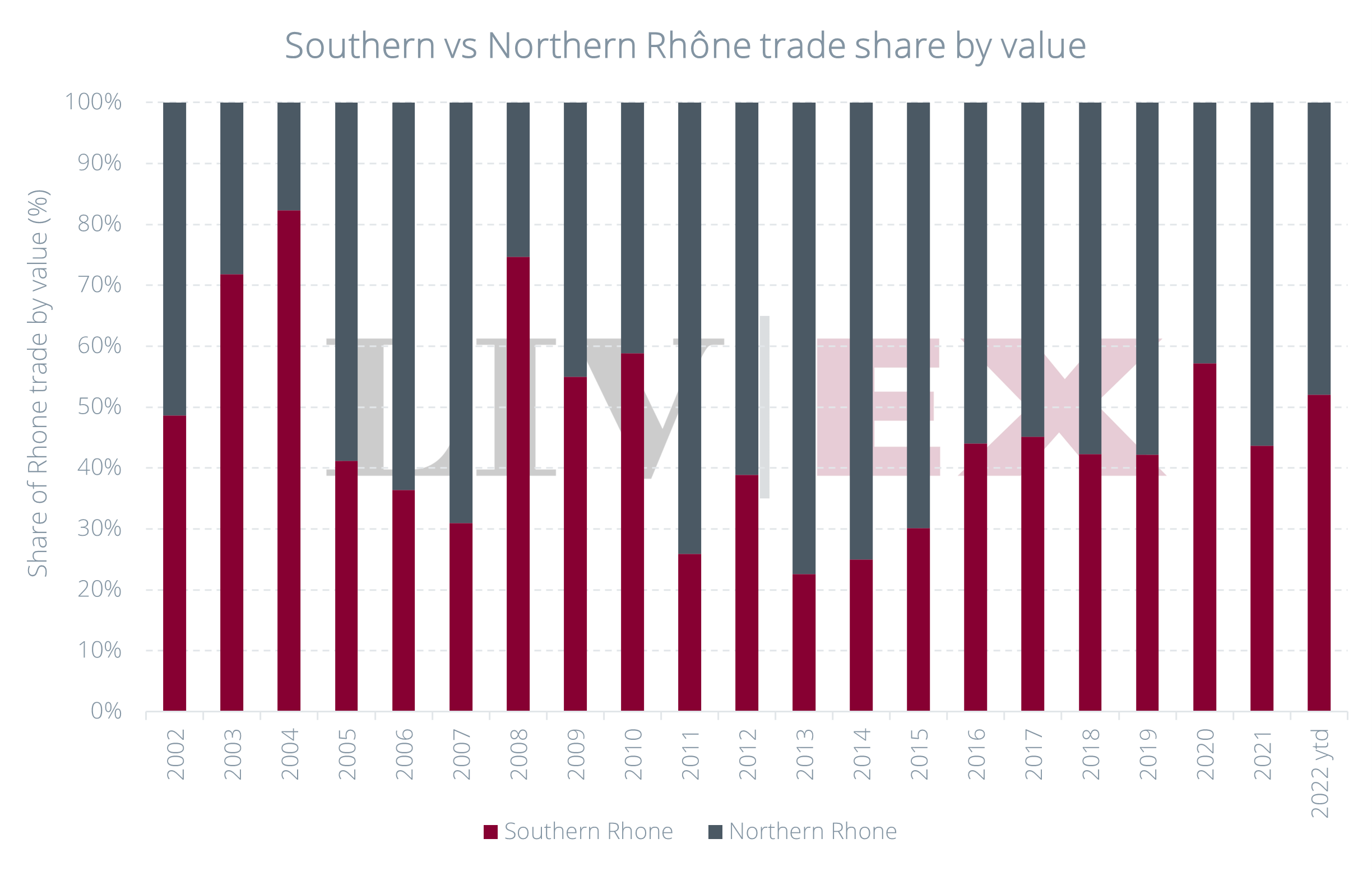

Châteauneuf-du-Pape wines have led the Rhône’s trading activity in 2022, accounting for 52.0% of trade by value. Although the northern Rhône appellations have led trade for the last decade, demand for the southern wines has been gradually increasing again since 2013.

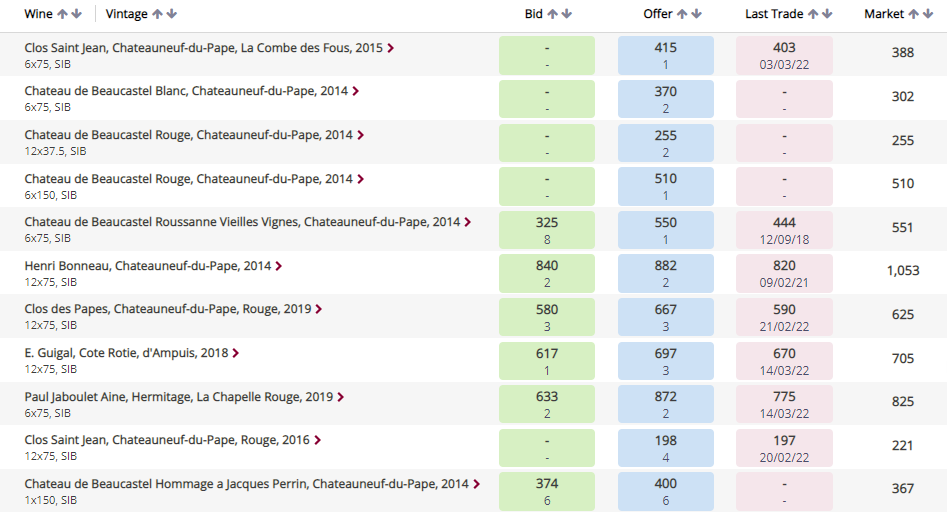

A record high of 785 Rhône wines (LWIN11s) traded on Liv-ex in 2021 and there are currently over 1,440 LIVE opportunities within the region, with offers starting as low as £35 per 6×75 case.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 560+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 16,000 wines. Independent data, direct from the market.