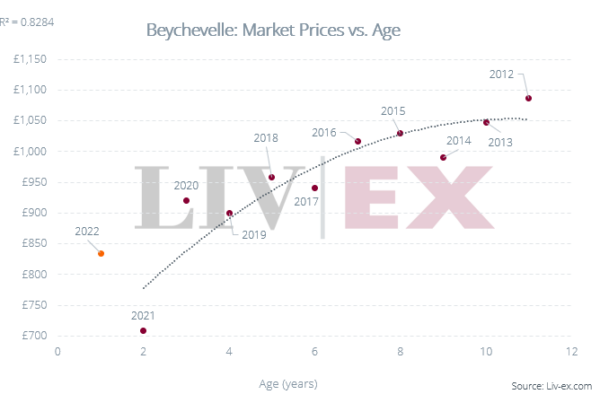

Print and read offline instead.

A strong start to the new year for fine wine

January was an active month for the fine wine market – the second best in terms of volumes traded in its history. Trade by value was dominated by Bordeaux (30.2%), Burgundy (24.6%), Champagne (10.9%) and the USA (10.4%).

Louis Roederer Cristal 2008 (with a Market Price of £3,620 per 12×75) was the most traded wine by value, while Daou’s Discovery Cabernet Sauvignon 2018 (£324 per 12×75) from Paso Robles led by volume.

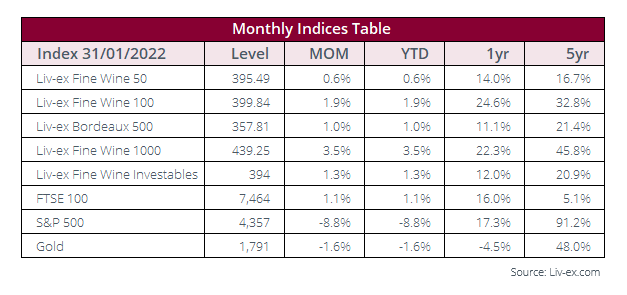

Fine wine prices continued their bull run into the new year, with a 1.9% move for the Liv-ex 100 and 3.5% for the Liv-ex 1000. Rising interest rates around the world are expected to dampen consumer spending, however, so it remains to be seen if fine wine proves resistant?

The market’s momentum was led by the Burgundy 150 index in January, which rose 6.4%. Heightened demand and impending shortages have contributed to persistent price hikes across the primary and secondary market, as examined in our recent report, Burgundy 2020: Stocks and sweet spots.

Additionally, eight out of the 10 biggest risers from the Liv-ex 1000 came from the region. Bouchard Pere et Fils Montrachet Grand Cru 2017 was the top performer. The wine has a current Market Price of £7,200 per 12×75.

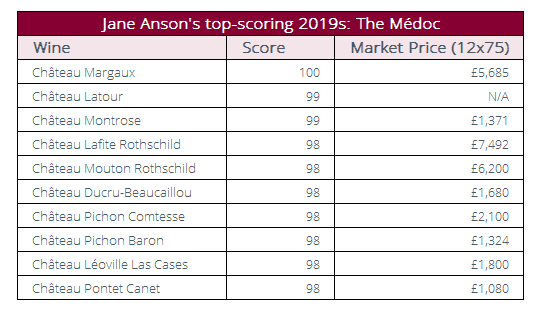

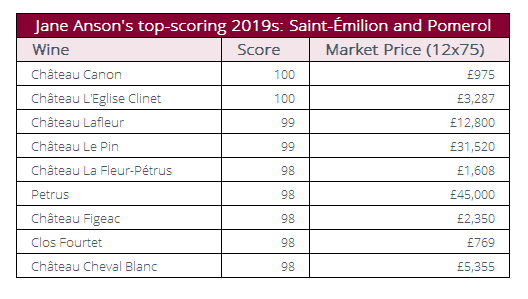

Jane Anson places Bordeaux 2019 alongside 2015 in terms of vintage quality

In her latest report on Bordeaux 2019 in-bottle, Jane Anson remarked that ‘this is an excellent vintage – not as consistently outstanding as 2016 or 2010 out of the past decade, but […] alongside 2015 (and in some cases 2018)’.

Anson suggested that 2019 could be seen as a winemakers’ vintage that was about ‘choices and selections’. For her, the successful wines were ‘extremely high quality and among the best of the decade’. She added that there was no clear Left/Right Bank split as both clay-limestone and gravel soils ‘did well’.

She awarded 100-points to one wine from the Médoc, one from Saint-Émilion and one from Pomerol.

From the Médoc, Château Margaux received a perfect score. She described it as ‘a signature Château Margaux, with so many different elements lending momentum and energy, and a feeling of effortless balance’. The wine has risen 35.3% in value since release. Anson further remarked that ‘the three wines of this First Growth [were] the most successful collection in any one Left Bank property this year’.

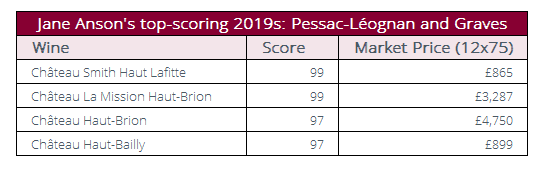

Over in Pessac-Léognan, Anson found wines that have ‘balance and ageing potential, with the reds slightly more successful overall than the whites’. She was impressed with the Smith-Haut-Lafitte stable, pointing out Le Petit Smith Haut Lafitte (94-points) as one of the value finds of the vintage, and awarded one of her two 99-points to Château Smith-Haut-Lafitte (rouge).

Anson found ‘some exceptional wines’ on the Right Bank too, awarding 100-points to Château Canon and Château L’Eglise Clinet, as well as two 99-point and five 98-point scores.

She noted, however, that the dry spring and hot summer led to wines with ‘high alcohols and extremely ripe fruit flavours in both St Emilion and Pomerol’ but that this was leavened ‘with real successes in clay-limestone soils that were able to keep freshness’.

When it comes to price performance, there is a near-equal split between the 80 leading estates that have risen and fallen in price since release. Find out more in our recent article on the best-performers and the biggest opportunities in Bordeaux 2019.

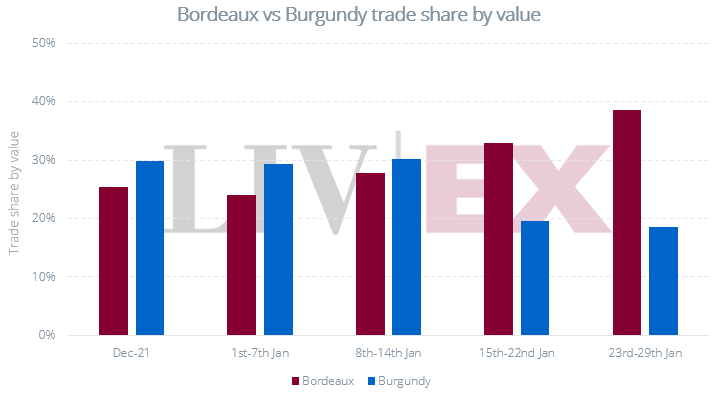

Burgundy overtakes Bordeaux in the early weeks of 2022

In late 2021 and the first weeks of 2022, Burgundy benefitted from Bordeaux’s sustained decline in trade share. Since mid-December, the two regions have taken nearly equal amounts of the market by value.

Burgundy overtook Bordeaux in December, a trend that continued throughout the first half of January. Bordeaux only rose above its 30% benchmark in the second half of the month to close January at 30.2% versus Burgundy’s 24.6%.

Burgundian trade, however, spanned 806 different wines (as measured by LWIN11s), while 705 wines from Bordeaux have seen demand since the beginning of the year. The ongoing market broadening within Burgundy itself suggests that the region is yet to unveil its full potential.

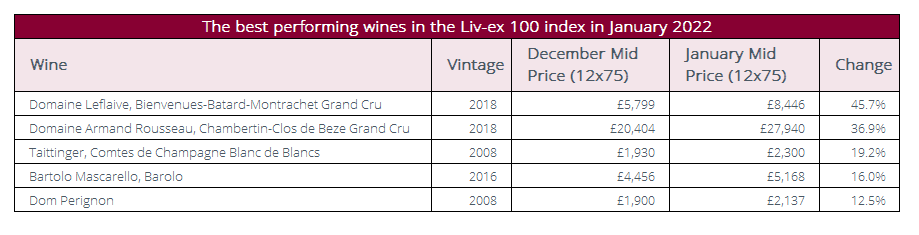

Burgundy 2018 and Champagne 2008 lead January’s price performers

January’s best price performers were a mixed bunch, dominated by Burgundy 2018 and Champagne 2008.

Domaine Leflaive Bienvenues-Batard-Montrachet Grand Cru 2018 and Domaine Armand Rousseau, Chambertin-Clos de Beze Grand Cru 2018 saw the biggest price rises. Other Burgundian 2018s that moved in value in January included Domaine Ponsot Clos de la Roche Grand Cru Cuvee Vieilles Vignes, up 6.7%, and Domaine Armand Rousseau Chambertin Grand Cru, up 6.6%.

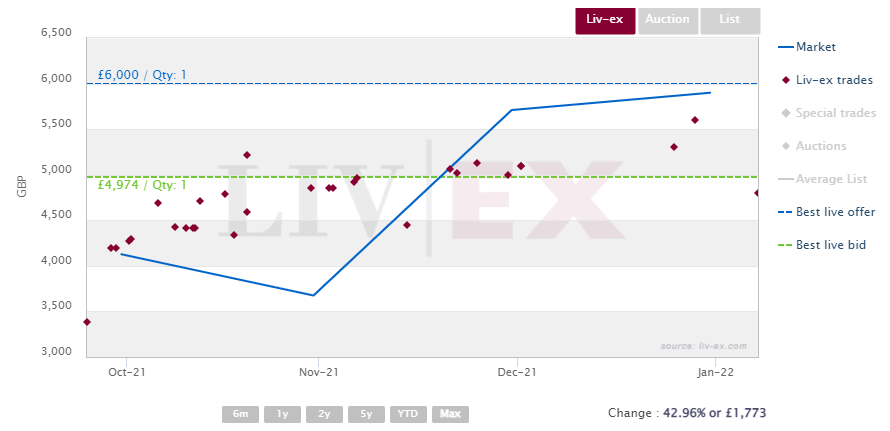

Major Champagne 2008 movers were; Taittinger Comtes de Champagne Blanc de Blancs, Dom Pérignon and Krug Vintage Brut. Krug, which was released in October last year, has already increased 43.0% in value. In the last month, the wine, which boast 100-points from James Suckling, went up 11.5%.

Krug Vintage Brut 2008 trades on Liv-ex

Industry news

OIV and WHO discuss health warnings on wine

Last week, the International Organisation of Wine and Vine (OIV) met with the World Health Organisation (WHO) to discuss health warnings that may soon be imposed on wine. As part of ‘a global strategy to reduce the harmful use of alcohol’ that WHO is expected to adopt, wine labels would have to state that ‘drinking causes cancer’. The new regulation could thus ‘see wine treated like tobacco, potentially putting an end to advertising and financial support for the industry,’ the drinks business has reported.

Wagram granted DAC status

As part of a wider amendment to Austria’s wine regulations, Wagram has become the country’s seventeenth DAC (Districtus Austriae Controllatus), according to Decanter. The region is adopting a pyramidal quality scheme, classifying its wines into Gebietswein (regional-wide wine), Ortswein (village wine) and Riedenwein (single-vineyard wine).

The secondary market for wines from Wagram is yet to develop, with just Anton Bauer Reserve Pinot Noir 2015 having traded on Liv-ex. In 2021, Austria’s trade by value was led by Mittelburgenland (57.2%) and Wachau (40.6%).

China’s ‘coercive’ trade tactics criticised

The UK, US and Australia have announced they will back a World Trade Organisation case against what has been termed China’s ‘coercive trading practices’. The case releates to Lithuania which has apparently been ostracised by China over its support of Taiwan. Wine Australia recently reported that China’s tariffs on Australian wine caused exports to fall by US$1 billion in 2021, with China-destined exports down 97% in value.

Ao Yun joins La Place

It has been announced that LVMH’s fine wine label ‘Ao Yun’ will be the latest non-Bordeaux wine to join the city’s négociant network, ‘La Place de Bordeaux’. It is the first Chinese wine to seek global distribution through the system. This will be handled by négociant CVBG, with the 2018 vintage due to be released on 30th March.

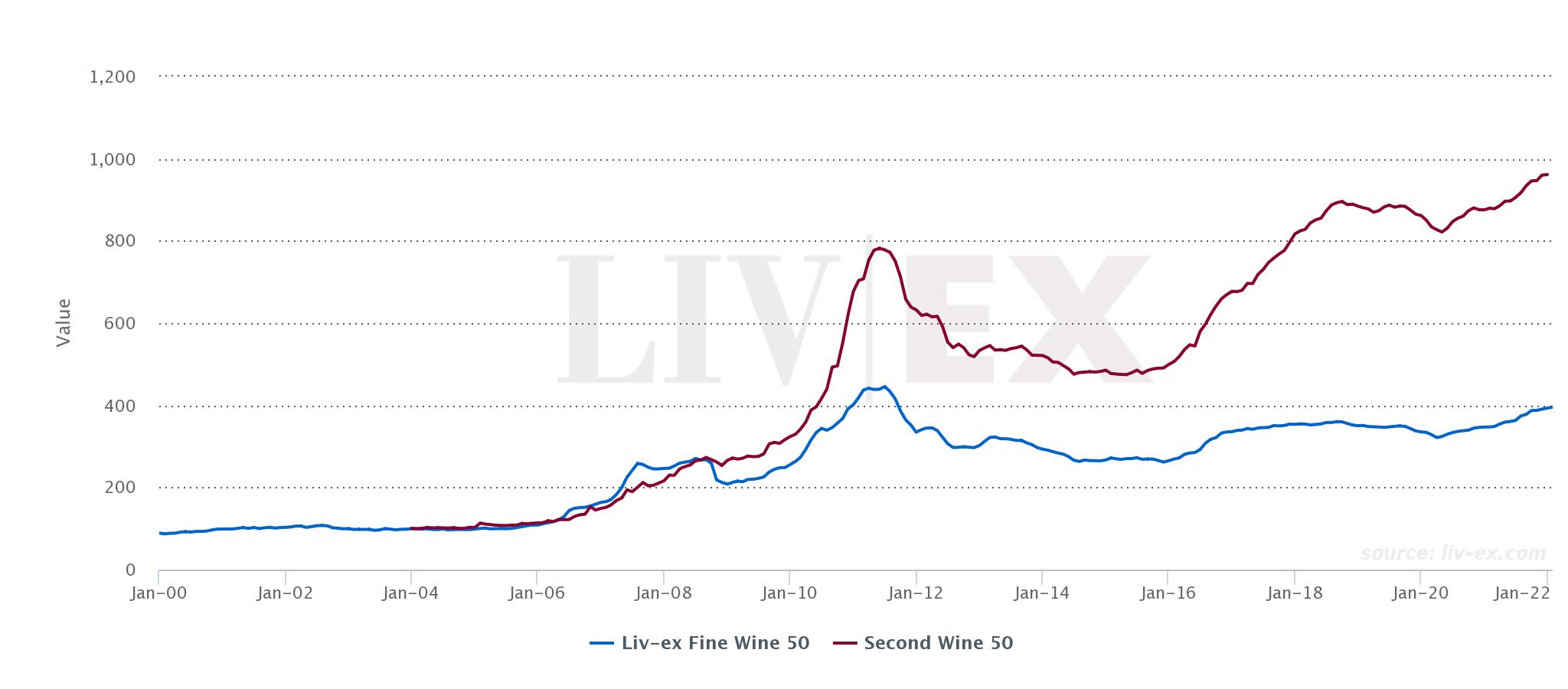

First Growth prices begin to outperform the second wines

In July 2019 we noted that one could buy 2.8 bottles of a second wine for the same price as a First Growth grand vin. This was down from a ratio of almost 6:1 in 2007.

The Second Wine 50 – one of the strongest sub-indices in the Bordeaux 500 – flourished between 2015 and 2019. From July 2015 to June 2019, the index rose 85.7% – although its strongest stretch was between July 2015 and September 2018.

In late 2019, when prices were at their peak, there was the combined storm of political unrest in Hong Kong and the beginning of the Covid-19 pandemic in Asia – a key market for these wines. Although the index began to recover in mid-2020, its level remained below its former peak. It was only in April 2021 that the index recovered fully from this knock.

While its level remains much higher than the Fine Wine 50, it is the latter that has enjoyed stronger price performances in the last two years (see table below).

Better vintages means larger price gaps

This strengthening of First Growths prices is starting to widen the gap between them and the price of their accompanying second wines.

As can be seen in the table below, the differences between first and second wine prices is often greatest in highly-rated vintages.

For example, the Château Margaux 2015 is currently seven times the price of Pavillon Rouge 2015. Although impressive, there are important factors to consider here. Margaux 2015 was not only released in a commemorative bottle but it was also the last vintage by the late Paul Pontallier, both of which have boosted its secondary market performance.

The 2010 vintages of Château Haut-Brion and Château Latour are also rare 100-point wines from Neal Martin.

The second wines from these vintages should not be overlooked, however. Despite their less impressive scores, Martin’s notes for these second labels are filled with praise.

He said, the 2015 Pavillon was, ‘pure joy, pure class’; the 2010 Forts de Latour ‘frankly puts some of the Grand Vins in the shade’ and the 2016 Clarence de Haut-Brion was ‘full of tension and terroir expression’.

On the other hand, some of the smallest differences in price can be found in ‘off’ vintages. Château Mouton Rothschild’s 2017 vintage for example has a Market Price of £4,316 (12×75), while the same vintage of Le Petit Mouton is £2,580. That’s just a case and half of Petit Mouton for one case of the Grand Vin. There is a similar closeness in the prices of Mouton’s 2013 and 2011 vintages

The ultimate problem for the second wines has always been that they are not the Grand Vins. The closer their prices got to those of their parent labels the less compelling they became. If the prices of the First Growths continue to rise and the difference between first and second labels continues to stretch, there will be opportunities for canny buyers among the second wines once again.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 560+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £100m of bids and offers across 16,000 wines. Independent data, direct from the market.