The UK government is proposing to make significant changes to the way excise duty on alcohol is calculated in the UK. The proposals are both unfair to wine drinkers and substantially increase red tape for wine merchants.

It is vitally important that both the UK wine trade and their customers write to their MPs and contribute to the consultation process, before the 30th January.

Background

The Government’s review of alcohol excise duty has been billed as a once in a lifetime opportunity to make the current regime fairer and simpler. Unfortunately, the model proposed by the Chancellor does neither.

The new system will tax wine drinkers 3x more than cider drinkers and 37% more than beer drinkers (on a per unit of alcohol basis) and massively increase the administrative burden on the supply chain (and SMEs in particular) by introducing 27 bands of taxation for wine.

This risks undermining the UK’s status as a major wine trading hub and missing a stated opportunity of Brexit to simplify regulations.

A breakdown of the changes and what they mean in practice

The changes proposed by the Chancellor focus on aligning duty rates according to alcoholic strength, rather than the type of alcohol. Under the current system there are three bands for still, sparkling and fortified wine, which is simple to apply.

The new system will introduce 27 bands by creating a band for every 0.5% of alcohol between 8.5% and 22%, with different duty rates for each band. This will mean ABVs will need to be checked for accuracy on all existing stocks held under bond in the UK and on any future arrivals.

Given the many hundreds of thousands of different products that Liv-ex customers trade and the many millions of cases that they hold in stock, this will amount to a very material one off and ongoing burden.

While the new scheme will reduce taxation for sparkling wine, duty on still and fortified wine will increase by an average of 20% and 30% respectively, collecting an additional £250m overall from wine drinkers according to the WSTA.

By comparison, duties for beer and cider drinkers will fall. Moreover, wine will be taxed at a higher rate per unit of alcohol – 26p per unit for wine, compared to 9p per unit for cider and 19p for beer.

This system is clearly both less fair for wine drinkers and more complex and costly to administer for the trade.

Smaller businesses face the biggest burden

The new regime will impact smaller businesses in the wine trade the hardest and threatens their traditional competitive advantage, which is to supply a wide array of artisan wines at competitive prices to customers.

Liv-ex alone has more than 100,000 different labels in its database and traded more than 12,000 different wines last year. Having to collect accurate ABVs on new and existing stocks for so many different wines will add a considerable new burden for merchants.

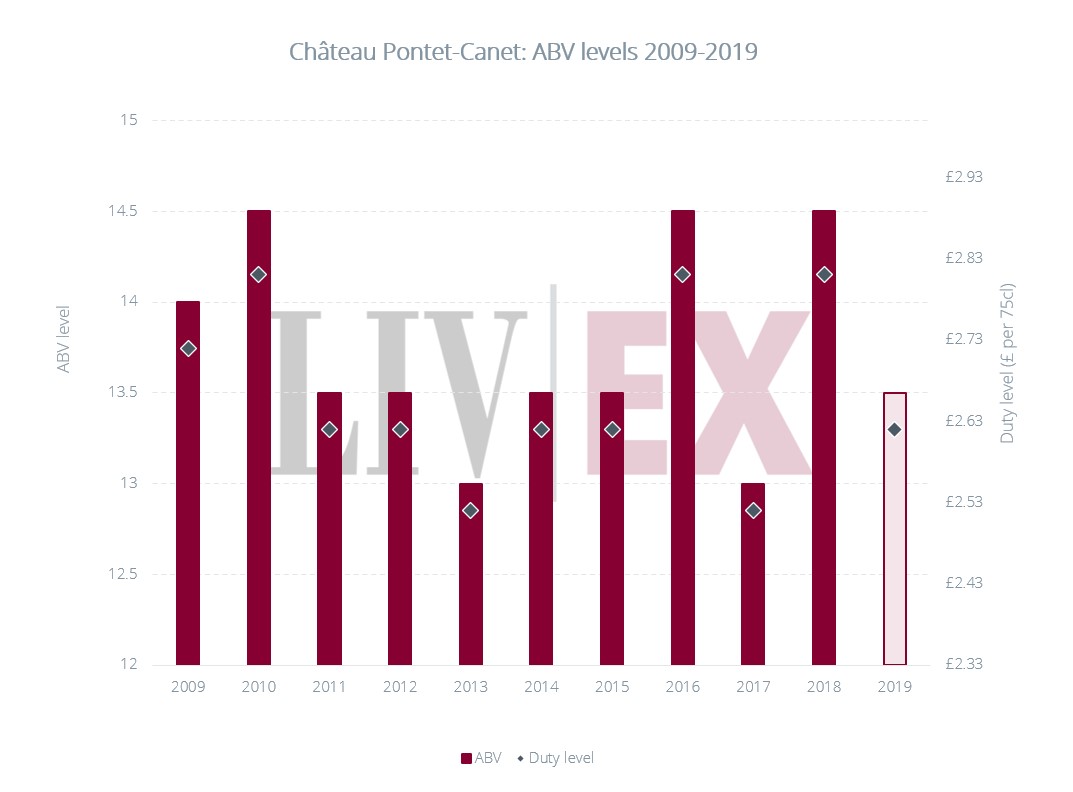

This problem becomes particularly acute when one considers the differences in ABVs for many estates from one year to the next. The chart below shows the change in ABV for Château Pontet-Canet and the corresponding duty rates that they would incur under the new system.

Under the old system these vintages would all have been taxed equally. Whereas, under the current proposals, these changes in alcoholic strength now span five distinct duty brackets.

Smaller importers, distributors and merchants, therefore, handling a wide array of wines will now have to check the ABV on every single line, every year to ensure that they pay the correct duty, placing a significant new administrative burden on businesses.

*ABV data taken from Liv-ex’s database.

There are two easy fixes for the Chancellor

- Reduce the differences between rates for different categories of alcohol and apply one basic rate per litre of pure alcohol to all categories of drinks. This really would be a fairer system than the current duty regime.

- Tax all wine between 8.5-15% abv at one rate fixed in the midpoint of the band (12%) and apply the same principle for fortified wines (tax all at 18%). This would maintain the principles of the Treasury’s proposal while reducing the bands of taxation from 27 to 2. This would be a genuine win and lift a huge administrative burden that current proposals would impose on the sector.

How you can help

The proposals are currently under a consultation period until 30th January 2022. It is vital that all UK wine merchants make their concerns heard by completing the consultation template on the Government’s website, sending it to [email protected], to [email protected] and to your local MP.

We would also like to take this opportunity to assure Liv-ex members that we are working hard to ensure that whatever the outcome, fine wine trading on the exchange can continue with minimal disruption. Liv-ex has already created a substantial database of ABVs for members to use should they wish. For more information, please contact your Account Manager.

Further reading:

- WSTA – Port and Sherry prices to rise.

- Harper’s – Time to act as duty deadline looms.

- Decanter – UK trade urges rethink on tax plans

- Liv-ex – Get wine commodity codes and ABV values easily with Wine Matcher.

About Liv-ex

Liv-ex is the global marketplace for the wine trade. Along with a comprehensive database of real-time transaction prices, Liv-ex offers the wine trade smarter ways to do business. Liv-ex offers access to £100m worth of wine and the ability to trade with 560+ other wine businesses worldwide. They also organise payment and delivery through their storage, transportation, and support services.