Print and read offline instead.

Fine wine returns to former peak

2021 is shaping up to be a strong year for the fine wine market, which is looking buoyant. The key phrases are ‘price performance’ and ‘diverse opportunities’.

2021 is shaping up to be a strong year for the fine wine market, which is looking buoyant. The key phrases are ‘price performance’ and ‘diverse opportunities’.

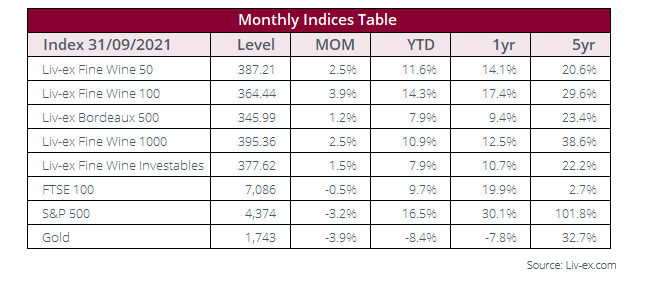

The industry benchmark, the Liv-ex 100, returned to a high not seen for a decade, while the broadest measure, the Liv-ex 1000, continued to climb to record levels. The Liv-ex 100 index rose 3.85% in September to close at 364.44, within a whisker of the summit attained in June 2011 (364.69). The Liv-ex 1000 is also at its highest level ever (395.37). Within its regional sub-indices, the Burgundy 150 was the best performer in September (and year-to-date), having now surpassed the record level set in November 2018.

The month was also dominated by news of brand new La Place releases, trade moves for major critics like Jane Anson and the sale of JancisRobinson.com, along with industry awards. The main event, the autumnal La Place de Bordeaux campaign, welcomed several Bordeaux estates and a growing collection of other European producers, as well as the usual New World wines. The most ‘successful’ release, as measured by secondary market activity, was Joseph Phelps’s 2018 ‘Insignia’ which topped trade by value in September.

The Napa Valley estate helped push the US’s September market share to 10.1% of the total, up from 6% in August. Italy, which also welcomed fresh releases, took 15.8% of total trade by value, just below its August share (16%). Bordeaux’s share dipped to 36.9%, while Burgundy increased to 22%. Champagne took 7.6% of the market by value, the Rhône 4.2%.

So far this year, the number of wines trading on Liv-ex this year is just 3% less than it was for the whole of 2020 (as measured by the number of LWIN11s trading). But, as recently explored, some regions like Burgundy and Italy have been subject to sustained broadening and have already surpassed their 2020 records.

News

St-Estèphe fourth growth Château Lafon-Rochet was sold by the Tesseron family to Jacky Lorenzetti. Owner of rugby club Racing 92, Lorenzetti is also the owner of Château Pedesclaux and Lilian Ladouys, as well as part owner of Château d’Issan. The sale is expected to be finalised by the end of the year.

A Nebuchadnezzar of Château Mouton-Rothschild 2000 set a new record at auction when it was sold for HK$1 million (US$140,299) by Bonhams in Hong Kong. The previous record, also set in Hong Kong, was HK$918,750.

Domaine Clarence Dillon has confirmed that it intends to incorporate the vineyards of the recently acquired Château Grand-Pontet into those of Château Quintus. Adding the 37 hectares of Grand-Pontet to Quintus will create a 42ha property, which will make it one of the larger classed growth estates in St-Emilion.

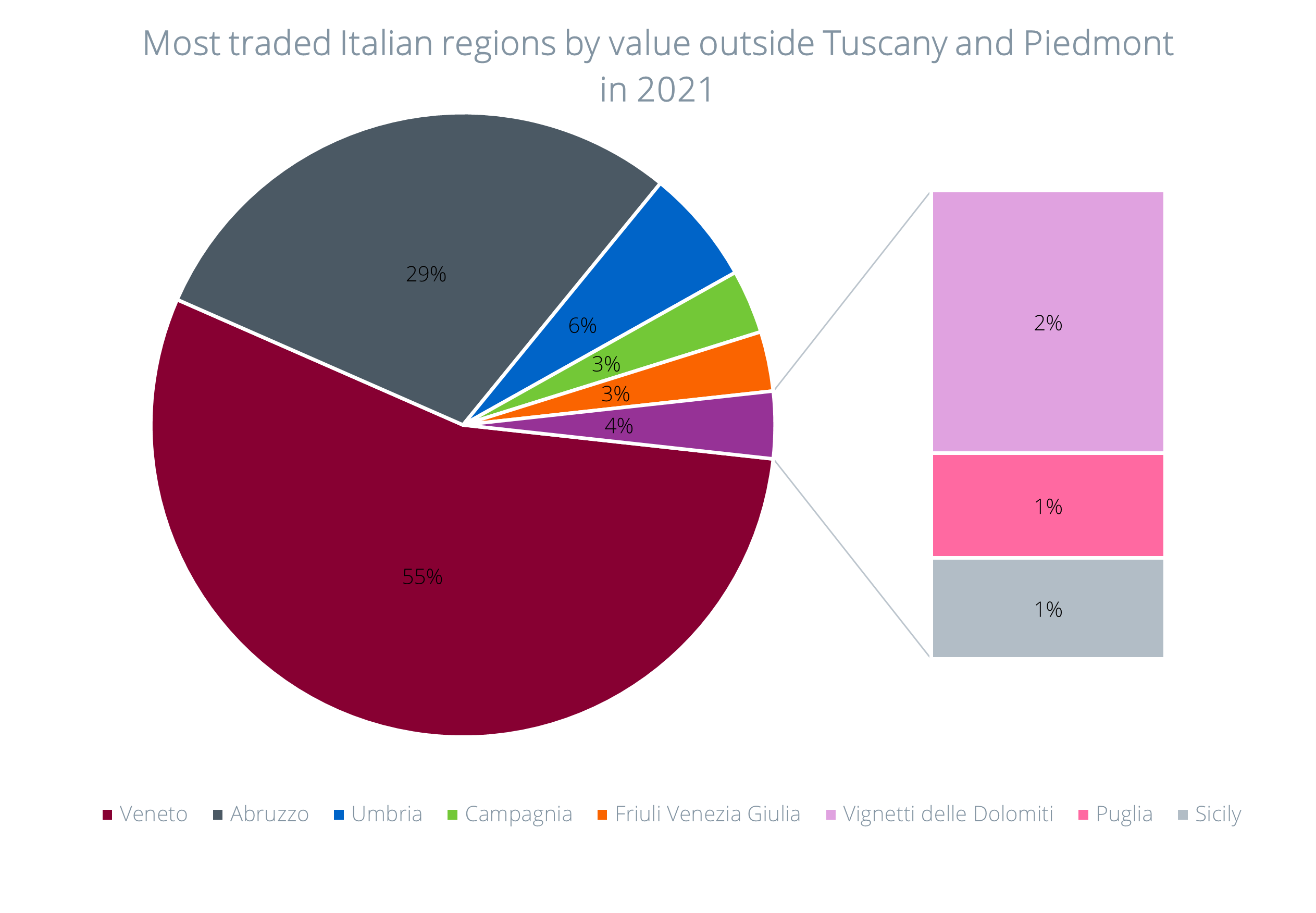

Chart of the month – The most traded Italian regions outside of Tuscany and Piedmont

Our short report on the diversified trade in Italian wine was published exclusively for Liv-ex members at the end of September.

A key theme was the increased presence of Italian regions outside Tuscany and Piedmont, which have traditionally dominated trade. In the past decade, Italy has seen a 2,566% increase in the number of wines entering the secondary market.

This month’s chart highlights the most traded Italian regions year-to-date, excluding Tuscany and Piedmont which together account for 96%. Although their exposure remains limited, and volumes traded are still very small, they are indicative of attitudes towards Italy’s enormous diversity and potential.

Veneto, the third-most traded Italian region, is most famous for production of Prosecco, but on the secondary market it has been its Valpolicella that has helped it gain ground. The first from the region on the global marketplace was for Dal Forno Romano in 2003, but, year-to-date, it is wines from Giuseppe Quintarelli that dominate activity.

Wines from Abruzzo have cornered 29% of the market for other Italian regions. Umbria has taken only 6% and its trade has been led by a white wine, Antinori’s Cervato della Sala. Other regions such as Puglia and Sicily have made up the remaining 10% of the pie.

So far this year, 16 wines from Campania have changed hands, compared to 11 from Sicily, and four each from Puglia, Trentino Alto Adige and Sardinia.

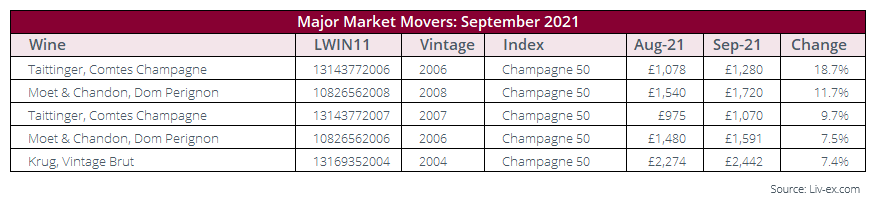

Major Market Movers– The biggest price performers from Champagne in September

The new records set in the fine wine market call for celebration. And there is plenty to choose from, new and old.

The new records set in the fine wine market call for celebration. And there is plenty to choose from, new and old.

This September saw two major Champagne releases – the latest 2011 vintage of Taittinger’s grande cuvée Comtes de Champagne, and the debut of Philipponnat’s 2012 Clos des Goisses through La Place de Bordeaux.

Champagne was also in the critical spotlight, as The Wine Advocate’s William Kelley released his latest scores on recent and forthcoming releases. The Champagne 50 was the second-best performing Liv-ex 1000 sub-index in September, up 4.5%.

A number of wines from Champagne were on the move. Prices for Taittinger’s 2006 Comtes Champagne (fifth most-traded vintage by value in 2021) and 2007 (second most-traded) rose 19% and 10% respectively. Dom Pérignon also featured among September’s biggest risers thanks to the price performance of its 2008 and 2006 vintages.

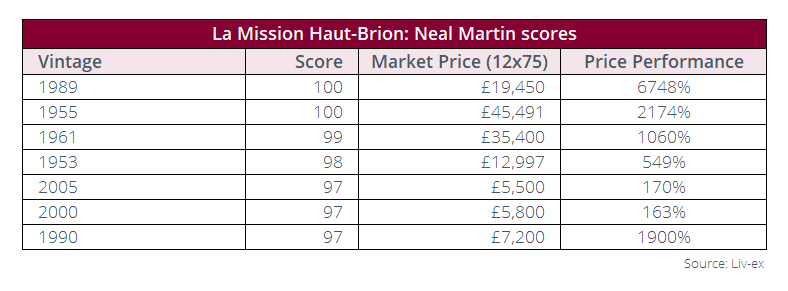

Critic’s Corner – Updated Neal Martin reviews on La Mission Haut-Brion

Neal Martin released an ‘armada’ of tasting notes on La Mission Haut-Brion for Vinous last month.

With Martin’s latest notes spanning the vintages 1928-2011, the publication now boasts a complete vertical of scores and notes for the property from 1957 to 2020. This now includes a review of the 1997, which had often frustrated Martin by its absence from previous verticals.

An estate he has long admired, Martin concluded his overview by saying that he believes La Mission is, ‘equal in breeding and complexity” to the First Growths and ‘would have had a chance of becoming a First Growth’ if it had been part of the 1855 Classification.

As can be seen from the table above, many of his top-scored wines have performed exceptionally well over the years.

Final Thought – Analysis of this year’s Bordeaux 2017 Southwold tasting

The annual Southwold Tasting, moved to a later than usual spot this year due to pandemic restrictions, was back in action at the end of September.

The 2017 vintage was under the microscope this year. After the strong 2015 vintage and highly lauded 2016s, the 2017s had a tough act to follow.

A better vintage than 2013, the growing season nonetheless started with a hard frost (causing some severe losses in places), and a cool summer meant there were high acidities and leaner fruit profiles.

The chief problem, however, was that after the blockbuster prices of the 2016s, prices for the 2017s were not cut as ruthlessly as many in the trade might have hoped.

The accompanying primeur campaign was a flop but does this mean the 2017s deserved to be condemned to the dustbin of memory? On tasting and reporting duty for jancisrobinson.com this year was Tom Parker MW.

He drew the distinction in his introduction between the outcome of the campaign and the quality of the wines.

Sales at the time were, he said, ‘poor’ – with some merchants selling 75% less than they had of the 2016s. On the other hand, his notes from the initial tastings compared the 2017s to the 2014s and, ‘in the case of the best wines, to a modern 2001’.

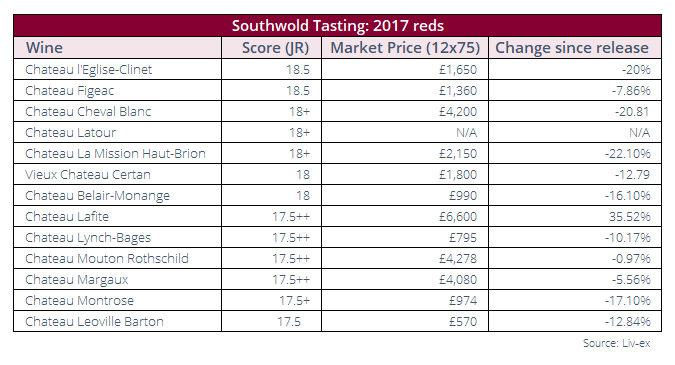

Tom Parker MW’s top-scoring wines from the 2017 Southwold tasting

The Right Bank came out of the tasting with some of the highest scores. L’Eglise-Clinet was broadly judged the favourite by the tasters.

In a vintage marked by high acidity, the richness of Pomerol proved a useful countermeasure to balance out the wines.

Parker added that the Left Bank didn’t have ‘the same peaks’ as the Right but there was ‘perhaps a touch more consistency’.

He said that Pessac-Léognan and Saint-Julien stood out among the appellations, and that there were bright spots in Margaux. Pauillac meanwhile was ‘up and down’ with the Cabernet showing a lot of ‘muscle’, while St-Estèphe ‘struggled to inspire us’.

The whites, however, were much more successful, both dry and sweet. The dry wines has ‘fulfilled their potential’, while Sauternes and Barsac, ‘excelled in 2017’ noted Parker.

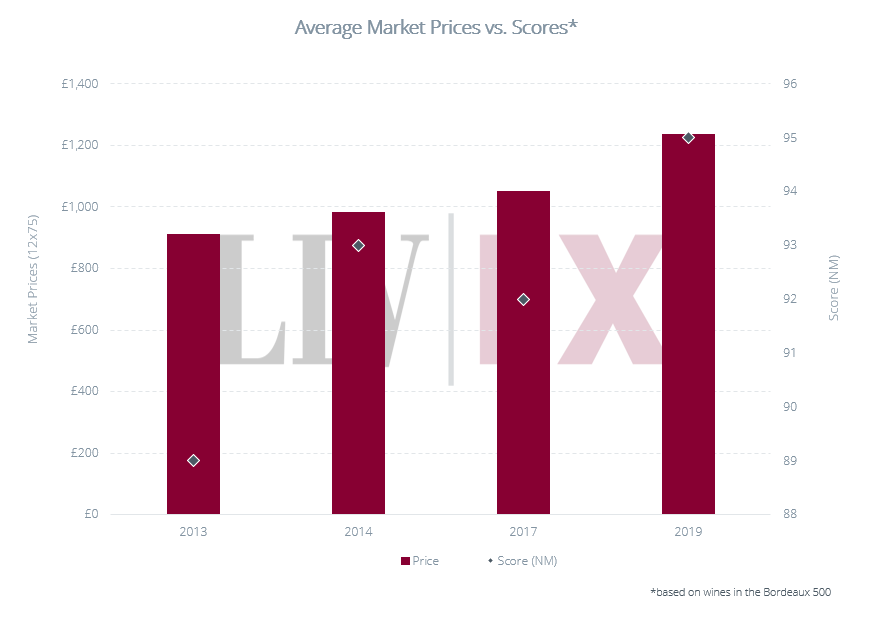

How do the 2017s compare to other vintages in the market?

Overall, Parker reflected that his initial view was largely unchanged though the Sauternes were ‘even better than I remember’.

The reds were more of a mixed bag and careful selection was needed, though ‘there are successes at every price point’. That said, while the best examples were pleasant enough, he added ‘I see little reason to fill up on 2017s that have not come down to be the cheapest vintage in the market other than 2013’.

So where do the 2017s sit today against those 2013s, as well as more favourably viewed vintages such as 2014 and 2019?

As can be seen from the chart above, on average the 2017s remain more expensive than the 2013s and 2014s in price. Currently a 12×75 case of 2017 has an average Market Price of £1,049; having declined 9% on average since release.

The 2014s, by contrast, cost £981 per case on average and have gained 50% since release. Take l’Eglise-Clinet as an example. The 2017 may have declined 20% to £1,650, but the 2014 is £1,200 and both (currently) have 95-points from Neal Martin. Is the 2017 still worth the £450 premium?