DRC might have stolen the headlines this year, but a number of non-DRC Burgundy wines have also traded actively in the secondary market. As we recently noted, Burgundy’s trade share has been growing without a significant boost from the iconic brand. Instead, other brands have started to become more active.

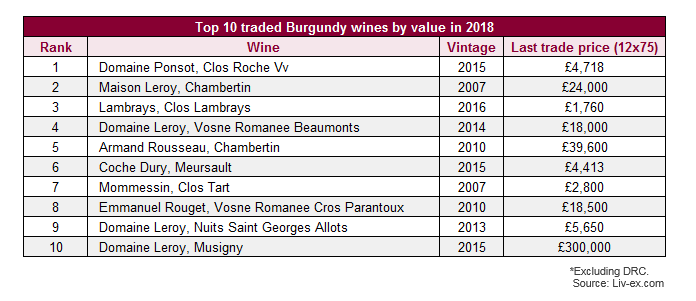

When looking at the top traded Burgundy wines by value, DRC dominates the table. Removing DRC, as we have done in the table above, allows us to explore broader Burgundy themes.

The top spot belongs to Clos Roche 2015 from Domaine Ponsot – the family estate, previously led by Laurent Ponsot, who exposed a multimillion-dollar counterfeit wine scheme.

The wine last traded at £4,718 per 12×75, 18.3% above its release price of £3,990 per 12×75. Still, our Ponsot Clos Roche Vv index – which tracks the performance of the ten most recent physical vintages – has been flat this year.

Four wines from Leroy also feature in the top ten – three from the Domaine (produced by the grower) and one from the Maison (its négociant business). The brand has proved popular among collectors and investors in the past year and has yielded an average price increase of 58.2%.*

The list above includes only one Chardonnay from the Côte de Beaune, Coche Dury Meursault 2015. The wine last traded at £4,413 per 12×75, just below its current Market Price.

The power of Burgundy

This year’s Power 100 has been dominated by wines from Burgundy and a number of the wines shown in the table above have topped the price performance rankings. You can read the report in the December issue of the drinks business. We will post our summary on the blog next week.

*Traded on Liv-ex in the last year (1st September 2017 – 31st August 2018). As calculated for the Liv-ex Power 100. A ‘brand’ is a group of wines made by the same producer. I.e. Lafite Rothschild produces the eponymous Grand Vin as well as Carruades Lafite.

[mc4wp_form id=”18204″]