Print and read offline instead.

Read the full article or jump to the relevant sections…

Key findings and facts

Key Findings

- Although the wines were generally rated better than 2018, the 2020s were not as strong as the 2019s.

- The 2020s were, on average, 27% more expensive than the 2019s.

- Stocks released continued to decline, with reductions of as much as 30% on some releases.

Key facts:

- Average UK release price per case 2020: £1,423

- Average Benchmark Critic score 2020: 94

- Largest ex-négociant price increase (per bottle): Petit Village, 97%

- Largest ex-négociant price decrease (per bottle): Pape Clément, -4.4%

2020 vs 2019

- Average UK release price per case 2019: £1,112

- Average Benchmark Critic score 2019: 94.9

- Average price difference per case 2019-2020: +27.9%

2020 vs 2018

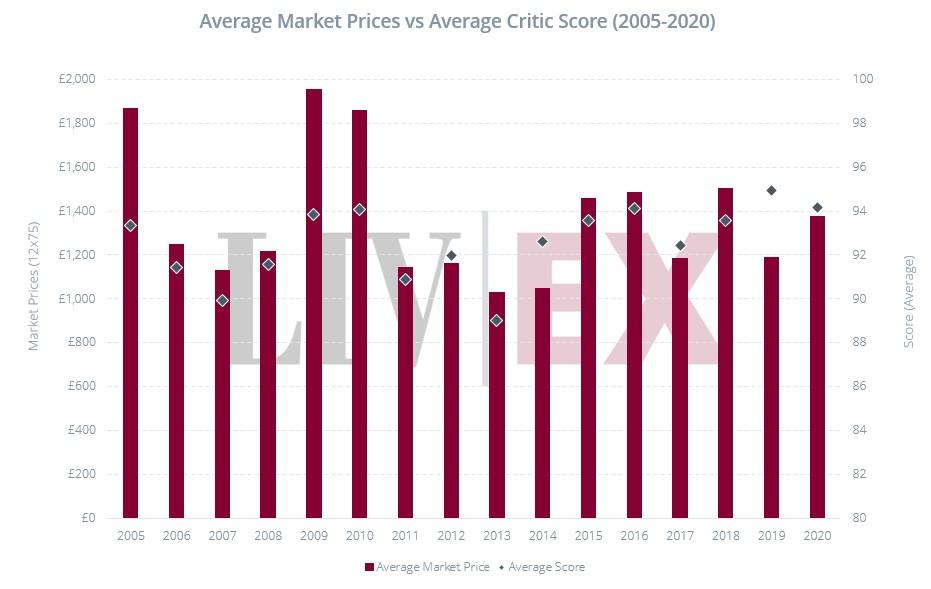

- Average 2020 UK release price vs. 2018 UK release price: -3.4%

- Average 2020 UK release price vs. 2018 Market Price: +2.4%

Summary

It was hoped that this year’s campaign would help reinforce the positive message of last year. The 2019s offered a raft of high-quality wines at appealing prices. In testing market conditions, not only were the wines enthusiastically received, new buyers were brought on board and a secondary market developed around sought-after wines (the first during a primeurs campaign in years).

‘The Magic is Back’ declared last year’s closing report. The introduction said: “With 21% price cuts on average, En Primeur felt livelier than ever. The cuts reawakened demand and rebuilt some faith in a system that had become an increasingly difficult affair for all involved.”

The margins for repeating this successful formula were always going to be tight. The market had overcome its pandemic shock and 2020 vintage was smaller than the 2019 and rumours swiftly circulated that price increases were on the way.

This was not an inherent problem, as long as price increases were in line with critical reviews of the vintage and continued to represent “Fair Value” to the end buyer. But did they?

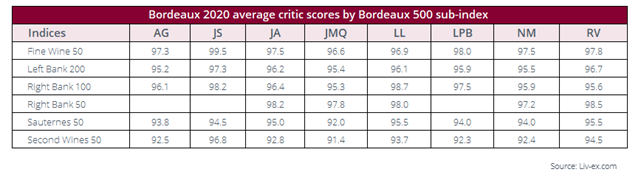

Scores: How does 2020 compare?

*Antonio Galloni, James Suckling, Jane Anson, Jean-Marc Quarin, Lin Liu MW, Lisa Perrotti-Brown MW, Neal Martin, Roger Voss

The 2020 vintage has widely been held up as the third in a “trilogy” of high-quality vintages, alongside the 2018 and 2019.

The major critics in their reports broadly seem to have ranked the trio in ascending order as: 2018, 2020 and 2019.

Benchmark Critic Neal Martin’s average score for the vintage was 94.2. This is above the 2018 (93.5) and on even slightly better than great vintages such as 2010 (94) and 2016 (94.1). It is still below the 2019, however, which with an average score of 94.9 is the best-scoring Bordeaux vintage.

The difference between the best 2020s and 2019s may, however, be “marginal”, Neal Martin suggested.

One group of wines that did not disappoint were the First Growths. At least one of either Lafite, Mouton Rothschild, Margaux or Haut-Brion featured as one of the top-scoring wines in the reports of Martin, James Suckling, Antonio Galloni, Lisa-Perrotti-Brown MW, Jane Anson, Jeb Dunnuck and others.

Initially, Martin rated the 2020 First Growths identically to the 2019s, with the exception of Margaux which he rated a little higher. He went on to rescore it 98-100 on a subsequent retasting in Bordeaux in late June – one of just two potential 100-points he awarded (Trotanoy being the other).

With the strength of the First Growths and other Left Bank estates revealed, the initial buzz about this being a “Right Bank vintage” subsided a little, although it is clear that many Right Bank estates produced excellent, score-topping wines in 2020.

“Don’t fall into the trap of believing that it’s a Right Bank or Merlot vintage – 2020 is far more nuanced and complicated than that,” warned Martin who said it was a vintage where individual terroirs excelled, not appellations.

That said, looking at the average critical scores according to sub-indices of the Bordeaux 500 – aside from the First Growths there was a marked tendency for higher scores in the Right Bank 50 and 100 compared to their Left Bank counterparts.

Pricing

Chart 1

No En Primeur campaign escapes the topic of price. Part of the appeal of the 2019s was undoubtedly the generous price cuts that accompanied them. The average reduction was just over 21% in the end.

Price increases were expected prior to this campaign. It began well enough though with the surprisingly early launch of Cheval Blanc. Released on 11th May, its initial offer of £4,656 per case was 3.5% up on the 2019 release but 2.7% down on that wine’s Market Price.

With this well thought out release it was hoped that Cheval Blanc was setting the tone for the campaign to come.

Although some subsequent early releases came with heftier premiums (Angélus increased its price by 13% ex-négociant for example), in the first four weeks of the campaign the average price increase was just 5.3%.

This was comfortably within the biggest pre-campaign predictions and elicited cautious hope from the trade.

As happened with the 2016s, however, prices began to spiral upwards in the closing stages. In the last week of the campaign when there were 28 major releases, the average price increase ex-négociant was 34%. This included the biggest increase on a 2019 release price, 97% from Petit Village.

Overall, the average case of 2020 offered in the UK was 27% higher than the 2019s had been, wiping out the cuts offered last year.

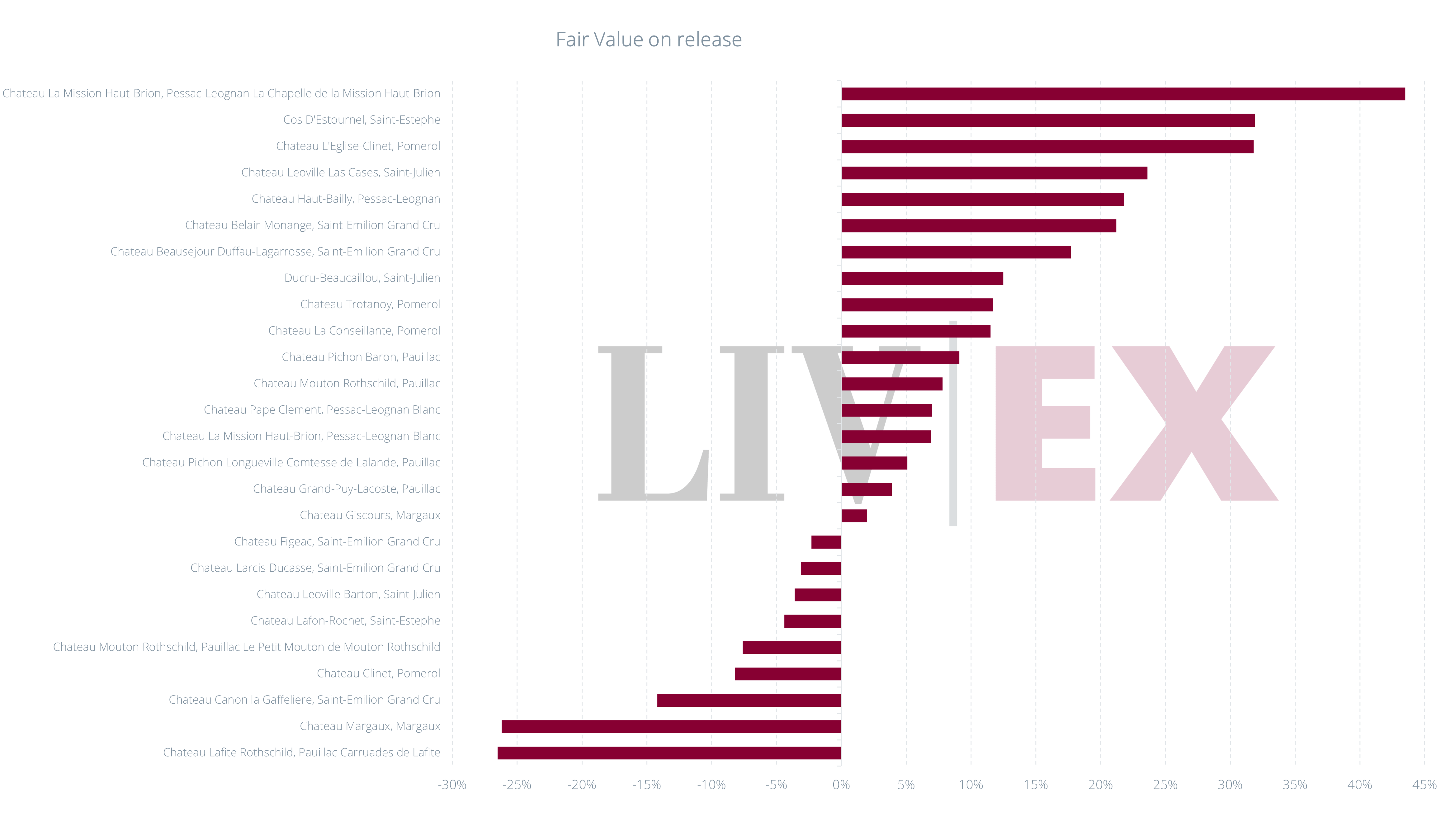

Where was the value?

Chart 2

Despite the price hikes, wines still managed to offer value. The First Growths in particular have enjoyed rising prices in the secondary market for many back vintages, not least their 2019s.

Margaux 2020 for example, with a 30% increase ex-négoce, looked very good value on release, and looks even better now following its upgrade to 98-100 from Martin.

Lafite’s second wine, Carruades, also came across as Fair Value, closely followed by the grand vin itself – though the asking prices for Evangile and Duhart Milon were much steeper.

Cheval Blanc’s early release is another clear example of a good value release. Clinet was another Right Bank estate that fell into this category of well-judged releases.

Several merchants also commented on the value Pavie seemed to show this year – and it was one of the very few major estates to keep its price the same as its 2019.

It looked a little over the Fair Value line according to the Liv-ex Methodology. Nevertheless, with a score of 95-97 from Martin, along with a 97-99 from fellow taster at Vinous Antonio Galloni and several other positive reviews, will have helped convince buyers they made a good choice.

Many other estates looked less compelling on paper. Though, as we shall examine further down, this did not at all prove a barrier to sales.

It is unarguable, however, that time and time again prices for 2020 only showed up what good value the 2019s both were and remain.

Stocks

The squeeze on stocks is a common theme of recent campaigns. It was noted last year that business was hampered by demand outstripping stocks made available.

Yes, 2020 was a smaller vintage than the current 10-year average but it was still comfortably larger than both the 2017 and 2013 vintages.

With the notable exception of Cheval Blanc (again), which increased the amount of stock it released by 20% on last year, the overall trend was ever tighter restrictions on volume.

Accurate figures are hard to come by, but reductions seem to have been 15%-20% on average. Haut-Brion’s reported reductions were 30%.

The consequences of this market manipulation have been made clear in previous discussions on this topic. Mounting stock “overhang” has a detrimental effect on both the En Primeur and secondary markets, reducing the incentive to buy and holding back price appreciation for many wines.

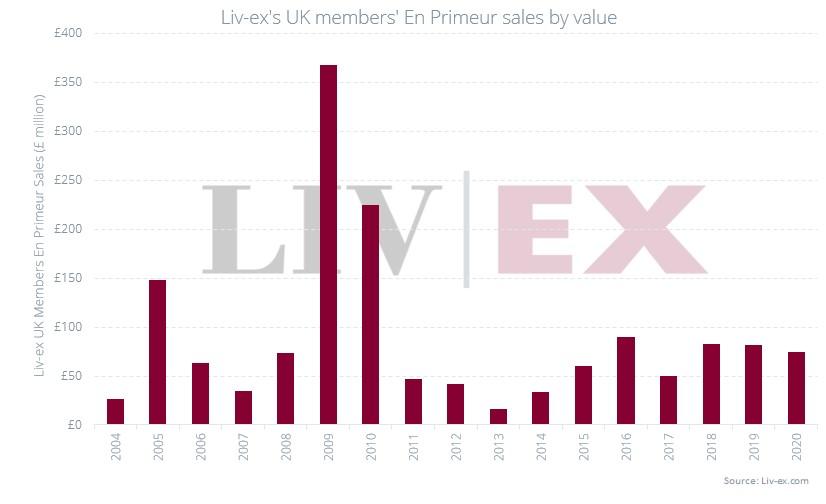

Sales

Gauging the temperature of the campaign from UK merchants, sales appear to have been a mixed bag. Cautious optimism at the start of the campaign had certainly soured by the end as prices rose as already mentioned.

Positive scores nonetheless created a buzz around certain wines and there was an undoubted appetite for wines on both banks, even if the Fair Value indications suggested the 2020 releases were not the best buy option. Then again, a lack of price sensitivity towards some wines may in part be due to the excess of unspent capital that has been hoarded during the past 16 months of lockdown and restrictions.

This was perhaps an underappreciated factor in the run-up to the campaign. It was broadly thought that circumspection would follow big price increases after the cuts offered last year. For buyers with cash to burn this clearly wasn’t the case.

But a lack of price sensitivity didn’t translate into an absolute tendency towards frivolous spending. There were many wines that were felt to be overpriced and whose sales were sluggish.

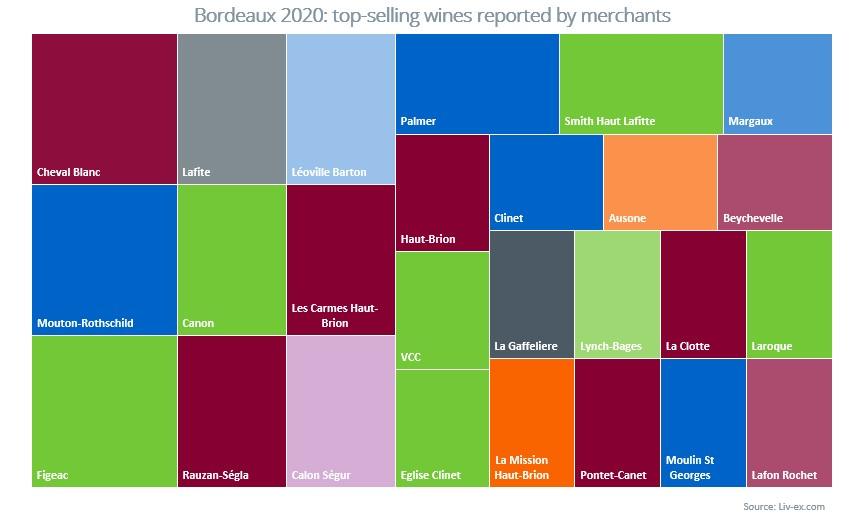

Best-sellers and wines that sold out (not always the same thing), seem to have broadly been centred around the “usual suspects”, First Growths and leading Right Bank estates, as well as an assortment of châteaux from both sides of the Gironde which are on the up (Figeac, Canon, Rauzan-Ségla, Carmes de Haut-Brion etc.). One will note the very close correlation of names in Chart 4 with those wines offering the best value in Chart 2.

A plethora of special labels marking various anniversaries and even, in one instance, a new cellar were announced during the campaign. This prompted activity from Asia, not a habitual player in the En Primeur game since the release of the 2010s.

That said, while some merchants clearly sold out of popular labels, offers for packs of wines, even First Growths, were still to be seen as the dust settled so not every wine “flew” everywhere.

The extent to which shrinking volumes contributed to wines selling through can only be speculative, but several merchants did report that they felt they could have sold a lot more of certain wines if the stock had been available.

There were many comments about the pacing of the campaign as well. After the rush at which last year’s campaign unfurled, this year’s certainly felt more sedate, though whether that or rising prices deadened appetites is open for debate.

On the plus side, aside from the busy gallop to the finish in the last week to week-and-a-half of the campaign, there was never a release flood. There was more time to digest each release in turn at least but, then again, if not every release looks immediately compelling, time to reflect too much can be a dangerous thing.

A final positive was that a good number of new customers tempted to partake in Bordeaux futures last year, do seem to have been retained.

Conclusion

It has become a sad mantra of En Primeur in recent times but this year’s effort was, once again, a missed opportunity.

Spiralling prices and restrictions in stock once again put the brakes on trade opportunities, frustrating what could have been a larger campaign by value and volume given that there was demand for wines across the board.

Having captured the mood of the market last summer and priced accordingly, it was noted in the opening report that keeping prices close to the 2019s was the sensible choice.

The market was in a far less vulnerable state this summer than it was last year and it had also broadened considerably. The need to offer compellingly priced wines was arguably even greater than it had been.

Furthermore, reports from the major critics repeatedly emphasised the point that 2020 was not a superior vintage to 2019. At best, Benchmark Critic Neal Martin was marking the leading wines of the 2020 vintage at the same level as the 2019s but in most cases he was scoring the 2020s lower than their 2019 counterparts.

Price increases of 20% or more for wines that are not rated as highly as less expensive wines released only a year ago will undoubtedly have many scratching their heads. There may have been a retention of new customers from last year, this is encouraging, but how many will stay if this pattern continues to repeat itself?

In years past, it was not uncommon for estates to keep prices the same from one year to another if quality was similar. Why was this option not pursued by more estates?

Instead, many châteaux readjusted their prices back to 2018 levels and, in the process, threw the value and quality of the 2019s into ever stronger relief. Those 2018s have largely declined in value post-release while the 2019s have generally risen; one can infer the likely trajectory of the 2020s from that.

It is an issue that will only compound criticism of recent En Primeur campaigns and that they continue to offer little to the buying chain as a whole, especially the end buyer.

Last year’s campaign rekindled a sense of the possibilities of En Primeur as an exciting and mutually beneficial business opportunity. With a few honourable exceptions, this campaign felt flat footed – a retrograde step.