Château Lafite Rothschild’s price premium versus the other First Growths tumbled from 129% a decade ago to just over 20% in 2017. With trade in the estate building, that premium is growing once more.

- After years of decline, Lafite’s premium versus the other First Growths is growing again.

- Lafite’s average case price is now over £7,000 compared to £5,000 for the others.

- The Fine Wine 50 – which measures the price performance of the First Growths – is slowly returning to its record level.

- Trade for Lafite in 2021 is already double what it was last year.

At the height of the China-driven bull market in 2010, Château Lafite Rothschild’s premium versus its fellow First Growths was 129%.

As that market declined and the fervour for Lafite died away, that difference went into decline. When Liv-ex last examined the ‘Lafite premium’, in January 2017, it had fallen to 24.6%.

As was reported last week in the Quarterly Review, the Liv-ex Fine Wine 100 is back to its record level set in the summer of 2011, while the Fine Wine 1000 continues to extend its foray into previously uncharted heights.

Falling prices of Bordeaux, especially for market leaders such as Lafite, helped spur the trend for a broader market and drastically cut Bordeaux’s overall market share by value (from 96% in 2010 to 40% in 2021).

With a broader base, the secondary market has returned to growth. But while Burgundy, Champagne and the Italian regions have benefited greatly from this, Bordeaux, the First Growths in particular, have not stood completely idle.

First Growth prices almost back to peak

The Liv-ex Fine Wine 50, which tracks the price performance of the 10 most recent physical vintages of the five First Growths, is slowly climbing back to its 2011 heights.

Closing September of this year at 387.21, it will take some time before the index reaches its June 2011 pinnacle of 448.38. Nonetheless, it has managed to rise 11% year-to-date and is up 20.6% over the last five years.

The First Growths were never going to be out of favour for long (if at all) and Lafite in particular seems to have returned to the embrace of collectors.

So far this year, Lafite is the most-traded wine by value in the secondary market and the second most-traded wine by volume.

Total sales of Lafite represent 7.5% of overall trade and are almost double total trade for the label in 2020.

The 2018 vintage is the most traded wine this year.

With such momentum behind it, it is no surprise to learn that the ‘Lafite premium’ appears to be growing once more.

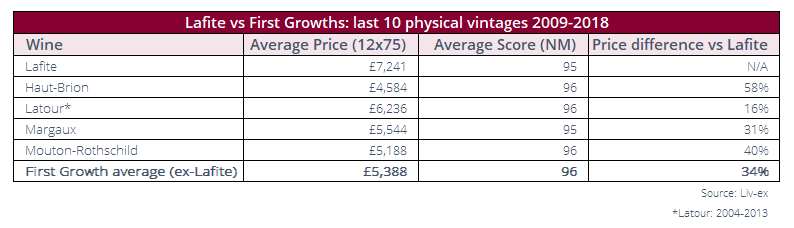

How do Lafite’s prices compare to the other First Growths?

Taking the last 10 physical vintages (2009-2018) into account, the average 12 bottle case of Lafite now has a Market Price of £7,241.

This is against a First Growth average (excluding Lafite) of £5,388*, a difference of 34%.

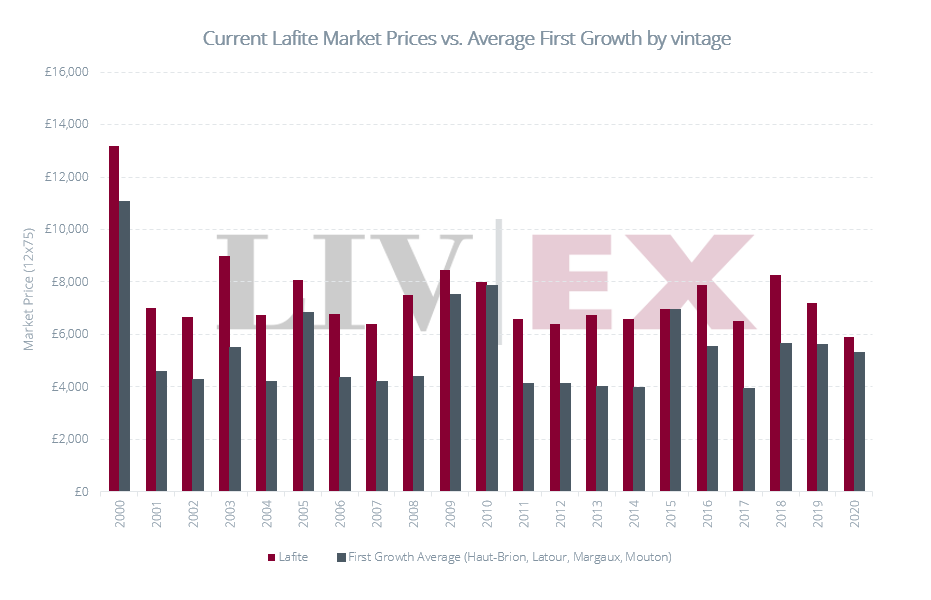

As can be seen in the chart above, for every vintage from 2000 to 2020, Lafite now costs more than the combined First Growth average. The closest the two come is the 2010 and 2015, where the prices of Latour and Margaux respectively bring the average up.

Even when examining prices at an individual château level, there are only four instances from the last 20 vintages where other First Growths carry a higher price tag.

These are: Château Mouton-Rothschild 2000, Château Latour 2009 and 2010 and Château Margaux 2015 – all wines with a very particular reason for their exceptional prices; Mouton with its Augsburg Ram design, the Latours with their 100-point scores from Robert Parker and Margaux for being the standout wine of the vintage in its bicentenary year

Price-score correlation?

Once again, Lafite appears to be in the good graces of the secondary market, and its premium is being re-established.

But does Lafite stand out in all areas? What of its average scores over the last two decades? We shall take a deeper look at this price to score ratio between Lafite and its fellow firsts in a follow-up post.

*with Latour’s vintages spanning 2004-2013 due to its release programme.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 550+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £90m of bids and offers across 20,000 wine markets. Independent data, direct from the market.

Not a member of Liv-ex? Request a demo to see the exchange and a member of our team will be in touch with you shortly.