The disparity between Lafite’s average scores and its average prices highlights the importance of brand power in the market.

- Lafite has one of the lower average First Growth scores yet continues to command the highest prices, highlighting the power of branding.

- Excluding Latour, Haut-Brion has the best average score over the last 10 physical vintages but one of the lowest prices, suggesting relative value.

A recent post examined the growing price premium for Lafite Rothschild versus the other First Growths.

After many years of decline, the difference between the price of Lafite and that of the average First Growth has recently grown to 34%.

But does the growing Lafite premium correlate with the scores its wines have received?

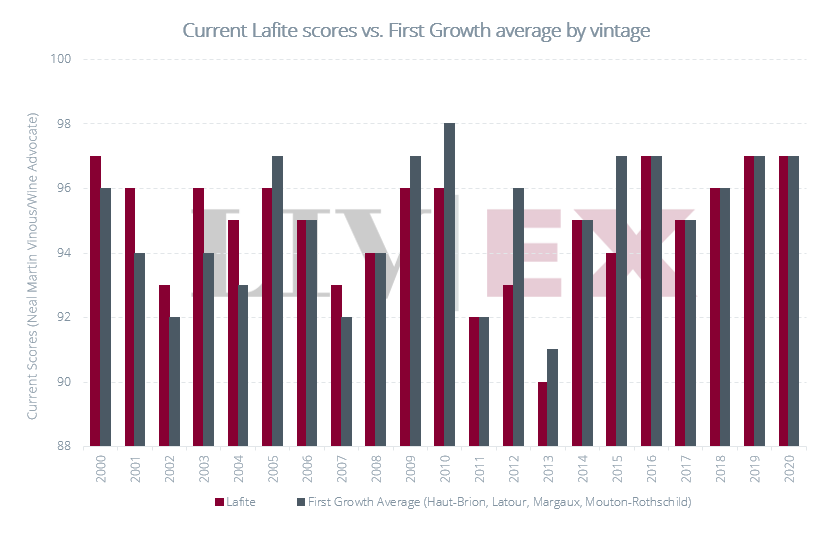

Lafite scores versus the First Growth average

When looking at the average scores for the First Growths, we looked at the most up-to-date scores from Neal Martin who is the ‘Benchmark Critic’ used by Liv-ex for Bordeaux.

Since 2000, his highest score for Lafite has been 97-points. The 2000 and 2016 vintages were both rated 97. The 2019 and 2020 wines currently have barrel ranges of 96-98, leaving the possibility open for a higher score – if you wanted to bet on Martin rating either wine higher than the 2000 or 2016.

As can be seen from the chart above, at the start of the new millennium, Lafite tended to have a better score than the First Growth average.

Towards the middle of the last two decades, the estate found itself outscored on several occasions before returning to close-to-parity since 2016 – or so it would appear.

Its rating of 90-points for the 2013 is now tied with Haut-Brion’s 2002 as the lowest score of any First Growth in the last 20 years (now that the 2000 Mouton-Rothschild has been upgraded from 89 to 91 in a recent tasting).

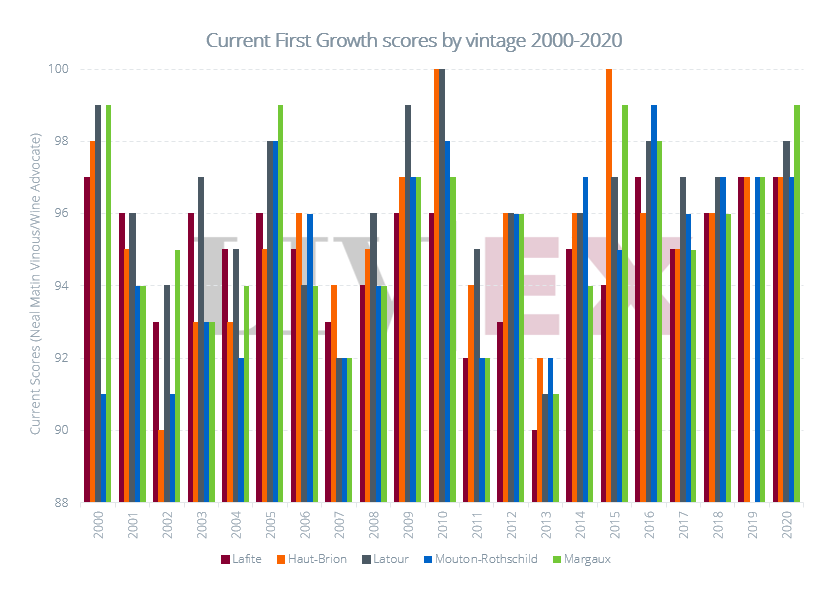

Scores of the last 20 years by estate

In the above chart, looking at each estate’s score by vintage, we can see that Lafite occasionally matches but never entirely out-performs the other First Growths on score.

On a few occasions – 2009, 2010, 2012 and 2015 – Martin’s score for the other firsts is higher than it is for Lafite.

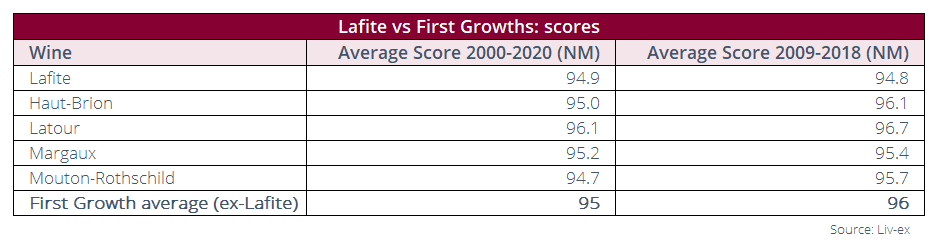

Looking at both the 10 most recent physical vintages and individual scores tells a different story yet again.

Average score comparison

Looking across the period 2000-2020 (see table), Martin’s average score For Lafite is 94.9, to the other Firsts’ 95-point average.

On an individual level, Lafite’s average score places it fourth, just above Mouton-Rothschild which has an average score of 94.7. Latour is the best-rated First Growth since 2000 with an average rating of 96.1.

As the table above shows, however, over the last 10 physical vintages (2009-2018) the difference between Lafite’s average score and that of the other four First Growths increases very slightly.

While Lafite’s average scores goes from 94.9 to 94.8, the scores of the other First Growths improve, with the average rising to 96-points.

Excluding Latour, which has only released wines up to the 2013 vintage, Haut-Brion currently stands as the highest-rated First Growth between 2009-2018.

It currently has some of the lowest prices among the First Growths as well. Its average Market Price for the 2009-2018 vintages is £4,584 per 12×75, compared to Lafite’s £7,241.

The importance of brand power

When considering Lafite’s growing price premium and the fact that it is the leading price-performer this year among the First Growths, it might come as a surprise to see that its average scores are not higher.

If anything, what this demonstrates is the power of a brand to override external factors. Lafite’s ‘pull’ and allure for collectors is strong enough to counteract the fact that it does not always score as strongly as its peers.

Liv-ex analysis is drawn from the world’s most comprehensive database of fine wine prices. The data reflects the real time activity of Liv-ex’s 550+ merchant members from across the globe. Together they represent the largest pool of liquidity in the world – currently £90m of bids and offers across 20,000 wine markets. Independent data, direct from the market.