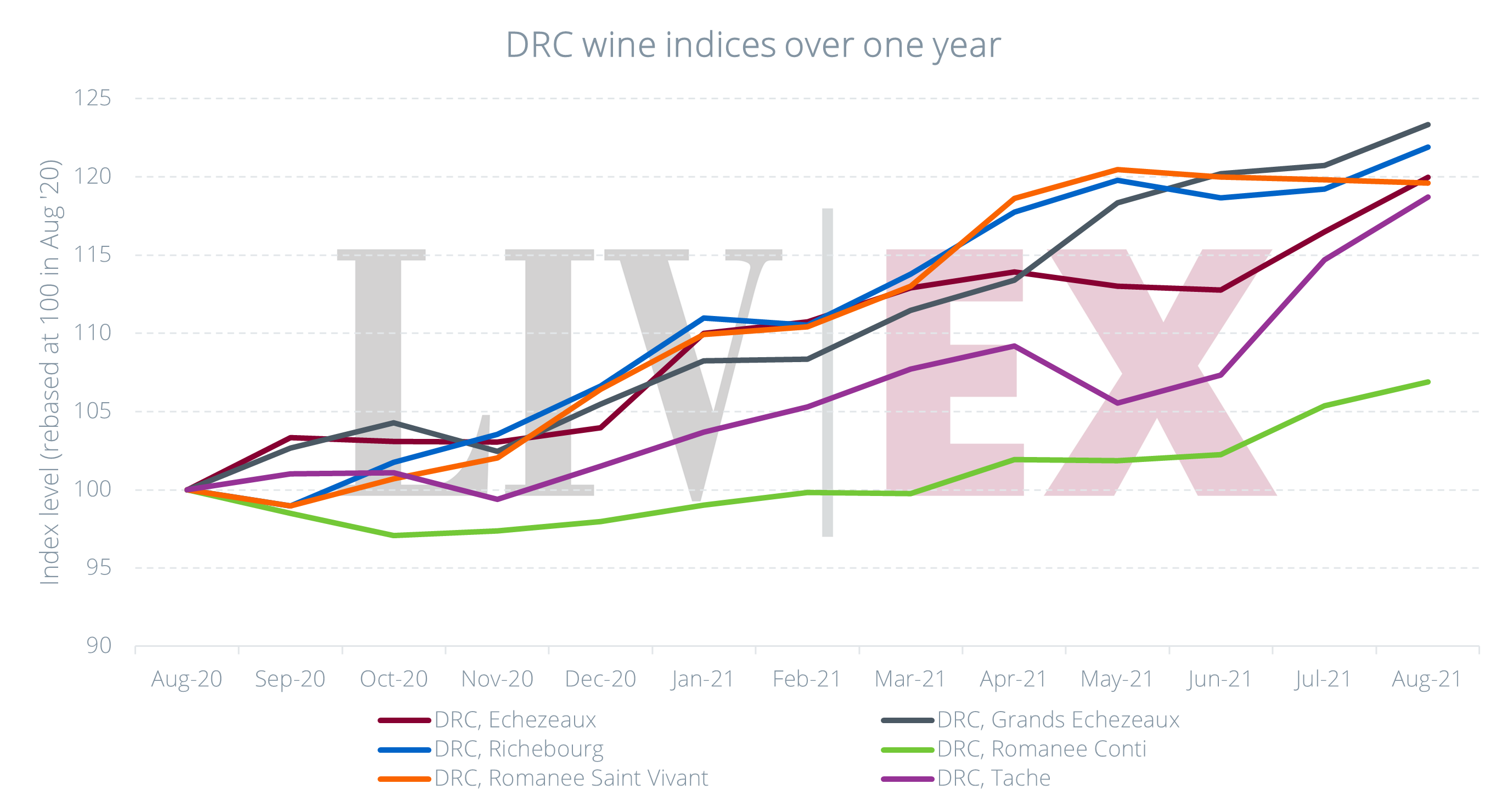

What is the direction of DRC prices in 2021 and which wines and vintages have traded the most?

- DRC Grands-Echézeaux is the best-performing DRC wine index in the past year.

- The generous and high-quality 2017 vintage has attracted activity across all DRC wines.

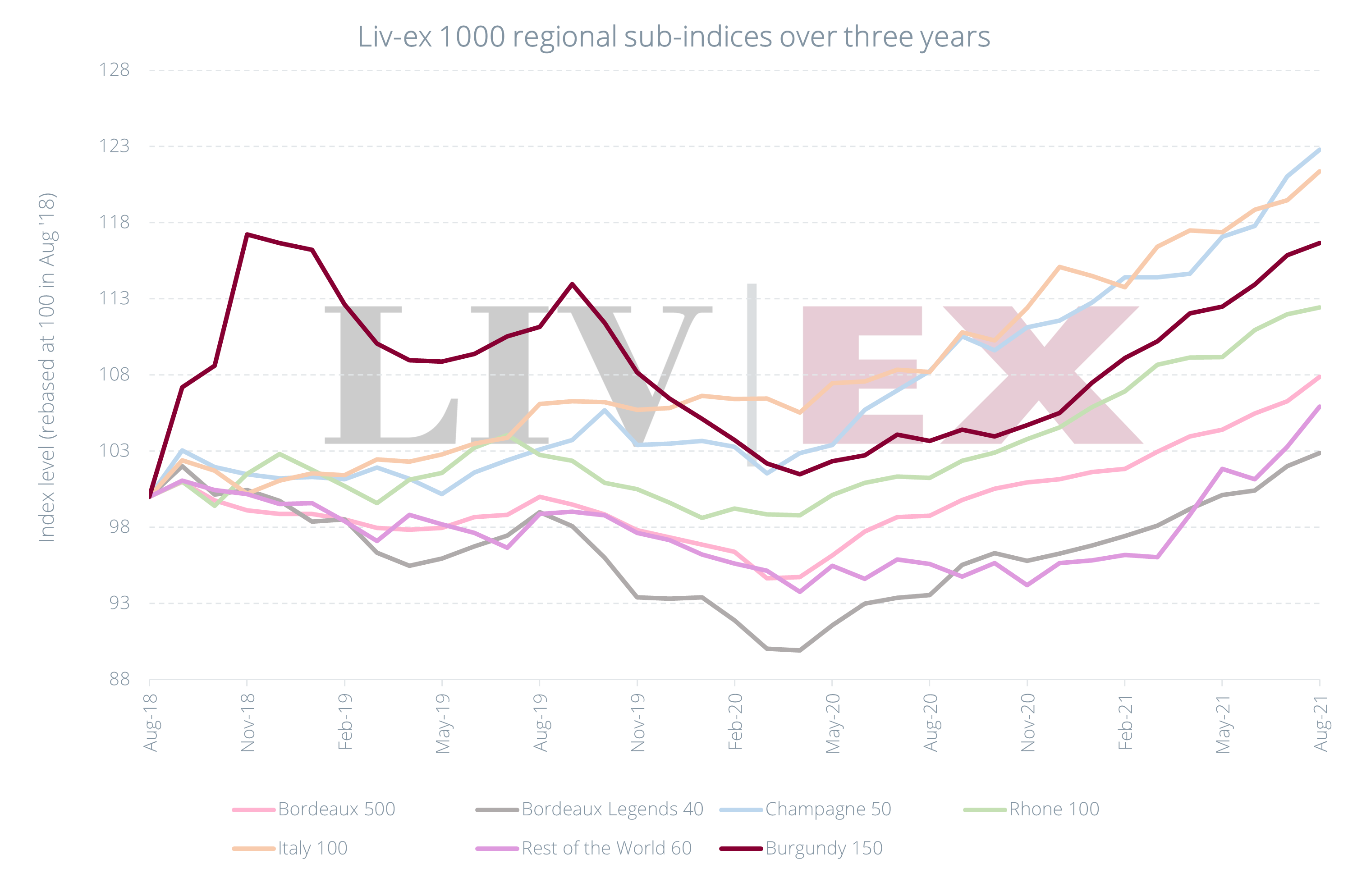

- The Burgundy 150 index is currently just 2.8 points off its peak (Nov. 2018).

The stable of Domaine de la Romanée-Conti is Burgundy’s highest echelon. DRC holds an indisputable collectible appeal and is the most traded Burgundian estate by value. It also topped the list of the most expensive wines, based on average trade price in the 2021 Liv-ex Classification.

What is the direction of prices in 2021 and which wines and vintages have been in buyers’ sights?

Price performance

Over the past year, all DRC wine indices have risen. All but Romanée-Conti have outperformed the broader market (Liv-ex 1000, 10.8%), the industry benchmark (Liv-ex 100, 14.7%) and the regional Burgundy 150 sub-index (12.5%).

The most expensive wine that the domain produces, Romanée-Conti, has been slowest to rise, though its index has still risen 6.9% in the last year.

Grands-Echézeaux has been the biggest riser, up 23.3%, having lagged behind in the longer term (it has been the second slowest mover since 2003). It has been followed by Richebourg (21.9%) and Romanée-Saint-Vivant (19.6%).

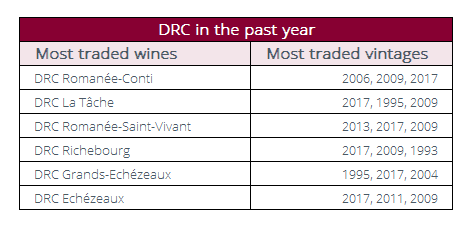

Trading activity

DRC Romanée-Conti, however, has led trade by value, and its 2006, which commands a Market Price of £191,400 per 12×75, has been the most active.

The 2017 vintage, which for the first time in years offered (relatively) high quantity and quality as judged by critics, has attracted activity across all DRC wines.

Broader trends

As the market for Burgundy has expanded (see our recent post on regional wine trade), DRC’s share of Burgundy has steadily fallen. DRC accounted for 54% of the Burgundy market 10 years ago; it now sits at a 15% share – a record low. Is DRC’s influence on Burgundy starting to wane?

Prices, however, continue to rise, both for DRC and Burgundy as a whole. The rarity that drives both would only seem to be enhanced by news of “historically low” yields in 2021. This has led to predictions for price hikes, but can Burgundy go any further?

As can be seen in the chart below, the Burgundy 150 index has regained lost ground in the past 18 months and is now just 2.8 points below its November 2018 peak. Will prices break previously set records by year-end? In terms of demand, measured by trading activity, the region already has.