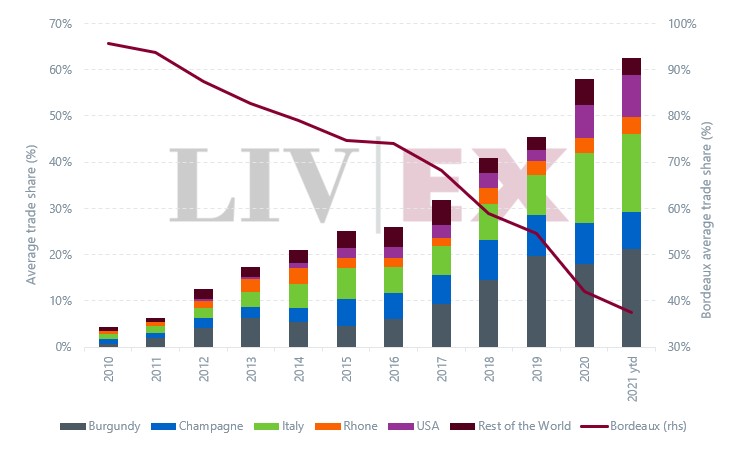

The big news of 2021 is how rapidly the fine wine market continues to diversify, as demonstrated by Liv-ex’s Fine Wine 1000. Bordeaux’s share of trade is less than half of what it was a decade ago, and interest in wines from Burgundy, Champagne, the Rhône, Italy and the US has grown exponentially.

Launched in 2014 as a companion to the benchmark Liv-ex Fine Wine 100, the Liv-ex 1000 tracks 1,000 wines in total and is the broadest measure of activity on the market.

Where the Liv-ex 100 tracks the 100 most traded labels by value month by month, the Liv-ex 1000 allows a much more granular overview of market activity.

And what it shows is interest in fine wines beyond Bordeaux has been rising. Interest in wines from Burgundy, Champagne, the Rhône, Italy and the US has grown hugely – while Bordeaux’s share of trade has shrunk.

Chart: Regional trade share by value

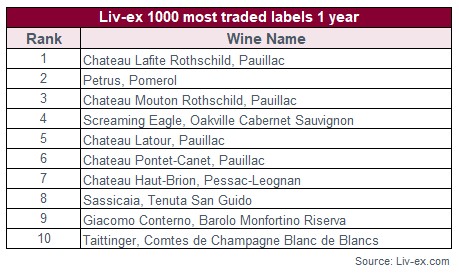

The number of brands traded on Liv-ex last year was 1,420 (up from 996 in 2019) while the number of total wines was 8,735 (up from 6,367 the year before). This was reflected in the 2020 Power 100, with a decidedly non-Bordeaux selection of wines in the top 10 positions and record new entries for labels from other regions.

In both January and February of this year the number of distinct labels (LWIN7s) traded each month has been over 1,000; if measuring each label with a vintage (LWIN11s) the number is over 2,000. March 2021 has also just become the broadest month of trade ever, with 1,250 distinct wines traded; 130 of them completely new to the secondary market.

The more wines that enter the market, the greater the volume of trading – and the greater the value. At present, there are more than £80 million worth of LIVE markets on the exchange. In this context, the Fine Wine 1000 is now a key tool by which the general health and direction of the secondary fine wine market can be determined.

Furthermore, the Liv-ex 1000 (as with all the Liv-ex indices) draws its data points from the number of live bids and offers being made on the exchange by a pool of 500 global fine wine merchants. It therefore represents the biggest and deepest pool of liquidity anywhere in the world.

Most importantly, as a resource it is completely independent.

What follows is a snapshot of performance trends.

Understanding the Liv-ex Fine Wine 1000

The Liv-ex 1000 has seven sub-indices: two for Bordeaux and one each for Burgundy, Champagne, the Rhône, Italy, and the ‘Rest of the World’. They were chosen based on their level of trade in the build-up to the creation of the index. The full list of wines can be found here.

Everything is measured by its price per 12-bottle (nine litre) case; the exceptions are Domaine de la Romanée-Conti which, due to its high prices and lack of liquidity, is measured on the strength of a single bottle and Petrus and Le Pin which are measured by three-bottle packs. Buying one unit of every wine in the index would cost £3,173,117 at today’s prices, which in turn are calculated using the Liv-ex Mid-Price.

The Liv-ex Mid-Price

This is the metric by which all the Liv-ex indices are measured. The Mid Price is based on merchant transactions and is calculated by finding the mid-point between the current highest bid price and lowest offer price on the Liv-ex trading platform. Each price is then verified monthly by our valuation committee, who consider all data at our disposal, including merchant offer prices and recorded transactions.

It is therefore the performance of wines in the market that dictates the ups and downs of each index. The Bordeaux 500 may represent half of the wines tracked by the Liv-ex 1000 but at present it only represents 32.6% of the total value of wines traded.

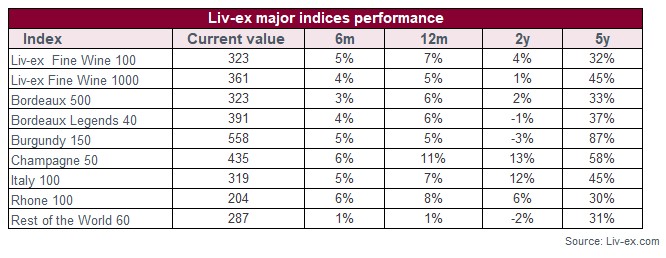

The Liv-ex 1000 performance at a glance

Due to the breadth and liquidity of its components and because it is driven by the activity of over 500 global merchants, the Liv-ex 1000 gives the best possible, independent, overview of the direction of the secondary market.

Between 2011 and 2014, the market for Bordeaux slumped, a sign that the Chinese-led bull market, fuelled by classed growth claret, was over. It has recovered, and that Bordeaux remains integral to the secondary market can be seen by how closely the Bordeaux 500 mirrors the progress of the Liv-ex 100, the former having risen 33% in the last five years.

But in the five years since February 2016, the Liv-ex 1000 has risen 45% to the Liv-ex 100’s 32%, which reflects the fact that more wines have been finding a market in the past five years.

In the last year, the various components of the Liv-ex 1000 accounted for 23.8% of total trade by volume on the exchange and 38.4% of total trade by value.

Moreover, because the Liv-ex 1000 is comprised of multiple sub-indices it is possible to break the index into its constituent parts, examine it in much more detail, and really get a feel for the nuances of the shift in buying trends that are taking place.

Burgundy

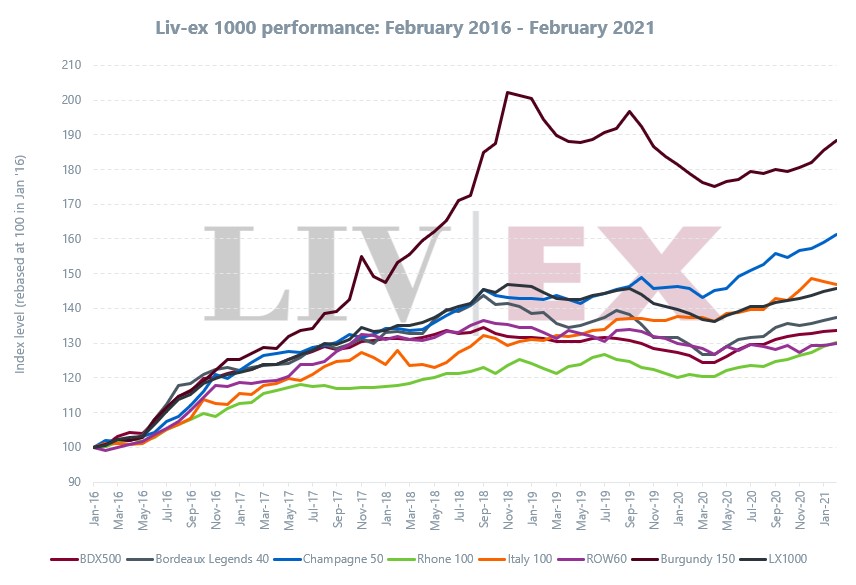

The most striking example of the changing dynamics of the market is the Burgundy 150. It has risen 87% over the last five years, the beneficiary of collectors putting their capital into a new category, after falling out of love with Bordeaux in the wake of the market’s decline.

The Burgundy index began to outperform both the Liv-ex 100 and 1000 as early as 2012, rising to a fever pitch in late 2018. At this point, spiralling prices and lack of stock for the most in-demand labels caused the index to come off the boil. It has been rising again over the past year, as buyers get behind different labels and growers such as Georges Roumier or Coche Dury.

You can read more about the market for Burgundy in our recent Burgundy Report, here.

Champagne

The Champagne 50 is another index that took off in the wake of the Liv-ex 100’s decline. It has risen 58% over the last five years, driven by the brand power and prestige of the grandes marques Champagnes, widely available stock, global distribution and accessible price points. Burgundy, Champagne and the Bordeaux Legends 40 are all out-performing both the Liv-ex 100 and their parent index at present.

Bordeaux Legends 40

The Bordeaux Legends 40 has a natural advantage over the Bordeaux 500, in that it is tracking a corps d’elite of claret. A red-coated phalanx with 100-point battle honours and famous vintages to prove their pedigree as their stock numbers increasingly shrink, driving up their value.

Italy

Then we come to the market’s new darling. The upstart Italy 100 has risen 45% over the past five years and is now at the same level as the Liv-ex 100 and Bordeaux 500. For drinkers used to France as their benchmark, the Super Tuscans provide the thrill of something new crossed with the comfortable familiarity of Bordeaux blends and Left Bank aesthetics, while there is also the Burgundian dynamic of Barolo with its single sites and inscrutable character of Nebbiolo to the get the little grey cells working.

The index has had a slow start to the year, there are often periods of rest after growth spurts as the market adjusts to new prices before kicking off again and it would be entirely unsurprising to see it start outpacing the Bordeaux 500 soon.

The Rest of the World

The Rest of the World 60 is an interesting index in that it includes American, Australian, Spanish and Portuguese wines.

It has risen 31% over the last five years. And while noise around American wines at present may lead you to think that the three US labels, Opus One, Dominus and Screaming Eagle are doing the heavy lifting, in fact the best performing wines over the past year have predominantly been Vega Sicilia’s ‘Unico’, Penfolds Grange and Taylor’s vintage Ports.

US wines in general are beginning to see a great deal of activity on the secondary market. As recently as 2019 trade in US wines represented just 2% of trade by value on Liv-ex, that shot up to 7% of total trade last year.

Although not part of the Liv-ex 1000, there is a California 50 index as well. Its performance over the last five years, as with other indices, has been stronger than some of its larger counterparts, rising 43%.

The Rhône 100

It would be unfair to call the Rhône 100 the ‘worst’ performer as over the five-year period in question it has risen 30%, which is almost as good as the Liv-ex 100. A recent report on the Rhône made clear that, although not spectacular, this French region has delivered slow but consistent returns while also representing the cheapest entry point into fine wine in the shape of Châteauneuf-du-Pape.

And like the US, it is an area with some momentum behind it at present. Its performance over the last 12 months was the second best after the Champagne 50 – rising 8% to the latter’s 11% – and both indices led the way over the last six months (each rising 6%).

A snapshot of the market

The stability and success of the market over the last half decade is directly attributable to its broader base.

Consider the Burgundy 150, which has seen such fantastic gains. If Burgundy had merely replaced Bordeaux as another market leader, then when Burgundy came off the boil in late 2018 and early 2019 – and declined 3% over a two-year period – there would likely have been a much greater impact on the Liv-ex 1000 than there was.

Instead, while the progress of the Liv-ex 1000 was undoubtedly hindered, it got through this hiccup with a rise of 1%, buoyed as it was by rises of 13% and 12% respectively from the Champagne 50 and Italy 100, plus smaller gains from other sub-indices.

Indeed, the fine wine market as a whole has recovered from its 2011 crash and every major index has risen over the last five years. Many indices are forging paths towards record heights, while the Liv-ex 100 is at its highest point in a decade.

Bordeaux continues to recover, but several obstacles hinder its progress. To begin with, there are many leading chateaux whose 2009 and 2010 releases, a decade later, continue to sit below their initial release prices while some other, ill-judged campaigns such as the 2017 and 2018 releases have also failed to hold their value between primeurs and physical release.

Then there is the issue of stock retention, with certain estates releasing less wine en primeur. This has not encouraged great gains in the secondary market as buyers are aware that what stock is out there is far from finite.

Bordeaux continues to offer many opportunities. Even with recent quibbles over pricing and stock, the great Bordeaux estates of the Left and Right Banks offer excellent quality wines, at what are, for the most part, affordable prices and with sizeable volumes.

The single index with the greatest number of wines with double digit performances over the last year is the Bordeaux 500. But it is also clear that while Bordeaux is still the engine room of fine wine it is no longer the absolute driver of the market as a whole.

New horizons

Comparing the Liv-ex 1000 to the Liv-ex 100 over the past five years, if they were rising in tandem then one could assume that a sub-index such as the Bordeaux 500 – which represents half the wines in the Liv-ex 1000 – was dictating the pace.

Yet they are not, and the reason for this has been the performance of Burgundy, Champagne, Italy et al. as buyers and collectors take an interest and pleasure in the world of fine wine beyond Bordeaux.

This interest is still in its early stages of development. Most Burgundy trade is concentrated on the Grands Crus of the Côte de Nuits, over 90% of Italian trade is focused on Tuscany and Piedmont, and 99% of US trade is Californian.

While it would seem unlikely that Emilia Romagna, the Côte Chalonnaise or Rogue Valley AVA could ever become juggernauts of the secondary market, there nonetheless exists tremendous scope for further development of these regions and countries. And, of course, there are the potential opportunities of Spain, Australia, Chile, Argentina, South Africa and Germany.

The market for fine wine is broader than ever. The Liv-ex indices will continue to evolve to represent the action and activity generated by the world’s leading merchants.

For more information on the Liv-ex 1000, click here.